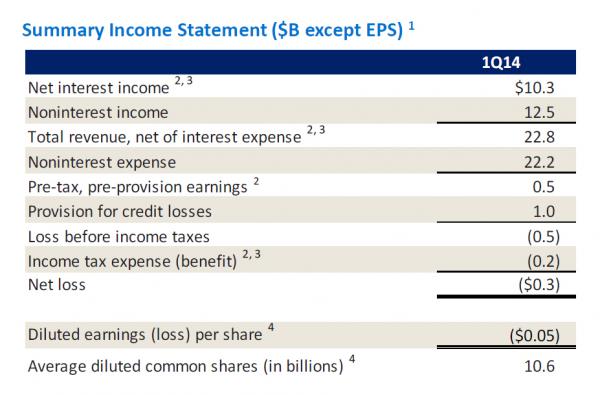

Moments ago Bank of America reported its Q1 earnings, and as expected, they were quite a mess, with the bank posting an actual loss of $0.05 on expectations of a $0.27 beat, which however – in the spirit of JPM – was the result of a $6 billion pretax charge related to various litigation items, which amounted to $0.40 per share. So Bank of America would like you, dear bank analysts, to do what you do to JPM every quarter with its recurring “non-recurring” litigation item, and please add it back.

These were the add backs:

- 1Q14 net loss of $0.05 per diluted share included pre-tax litigation expense of $6.0B, or $0.40 per share after-tax

- $3.6B pre-tax expense associated with previously announced FHFA settlement

- $2.4B pre-tax expense for additional reserves primarily for previously disclosed legacy mortgage-related matters

The only good news at the P&L level was that the Q1 reserve release was “only” $379 million, down from $804 million in fake earnings a quarter ago.

But what is worse is that Bank of America reported Net Interest Income of $10.1 billion, far below the expected $11 billion, and an amount that had nothing to do with legal fees, “one-time” charges and reserve releases.

Why was this number so weak? Because not only does BofA’s balance sheet continue to collapse, with its mortgage services portfolio crashing from $1.185 trillion to just $780 billion, but because BofA just reported the lowest NIM, or Net Interest Yield as it likes to call it, in history at 2.29%. So much for that NIM surge that everyone was expecting.

And speaking of BofA’s balance sheet things turned decided sour in Q1 when the bank’s provision for credit losses – an amount that flows directly through the P&L – soared from$0.3 billion to $1.0 billion, the highest since Q2 2013.

As the bank explained, “Provision for credit losses increased from 4Q13 due to slowing pace of credit quality improvement.” Alternatively, one could call it what it is: an increasing pace of credit deterioration, hence the loss provision surge.