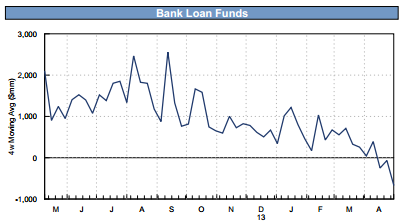

After several years of frenzied buying (see post), corporate loans have fallen out of favor – somewhat. Fund flows have turned negative,

Source: Goldman Sachs

… and performance on a total return basis has flat-lined. Over the past six months, HY bonds have outperformed sub-investment grade senior loans by some 1.75%.

Blue = HY bond ETF total return, orange = senior leveraged loans ETF total returnÂ

(source: Ycharts)

FT: – Ninety-five consecutive weeks of inflows to US funds that invest in leveraged loans made by banks came to an abrupt halt in the second week of April, when investors pulled $249m from the market. Since then, investors have continued to withdraw money from the funds, taking out $664m just last week, according to Lipper data.

Why all of a sudden? Here are some reasons:

1. With the average leveraged loan yield dipping into the 4.5% – 4.75% territory a couple of months ago, some investors felt the asset class is too richly priced. This is a sub-investment-grade product owned in part by some trigger-happy and often uninformed retail investors who loaded up on BDCs, senior loan mutual funds, loan closed-end funds, and loan ETFs. For some it was time to lighten the exposure.

2. After the recent default of Energy Future Holdings, otherwise known as TXU (the largest leveraged buyout in history), the notional-weighted loan default rate spiked from 1.2% per year to 4.6%. That’s right, one deal changed the historical default rate that much because of its size ($40bn in bonds and loans). Some investors got spooked by TXU and the realization that leveraged companies can and will sometimes default (surprise!) – even though the TXU default/restructuring has been expected for quite some time.

3. Related to the item above, some investors have become a bit uneasy with deteriorating credit quality in the space. The market has had a tremendous increase in the so-called cov-lite deals …

Source: Merrill Lynch