In spite of what appeared to be an improvement in China’s manufacturing sector (see chart), China’s economic picture remains cloudy. A number if indicators point to rising uncertainty and slowing industrial demand.Â

Investors are becoming increasingly uneasy with the nation’s property markets, which JPMorgan called “a major macro risk”. Volumes of unsold real estate are now at record levels and sales continue to slow. Nomura’s researchers are convinced “that the property sector has passed a turning point and that there is a rising risk of a sharp correction”. Of course since the authorities can easily intervene, the situation may not be as dire as Nomura predicts. Nevertheless, the nation’s property markets continue to pose significant risks.Â

Moreover, some high frequency indicators are once again flashing warning signals. According to the ISI Group research, exports to and sales in China by US corporations have turned materially lower after remaining stable since early 2013 – indicating weakening demand. Anecdotal evidence suggests that a similar slowdown has also occurred for Japanese and euro area firms selling to China.

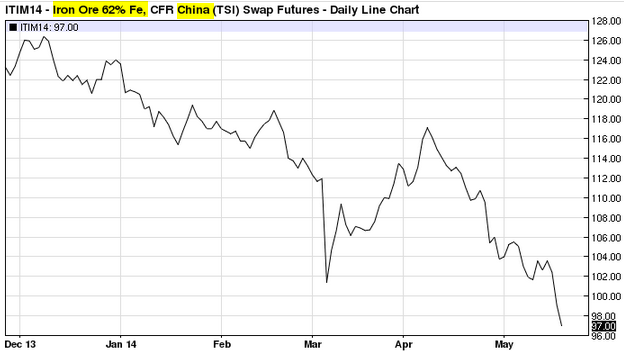

The most worrying indicators however are the key industrial commodity prices. Futures on iron ore sold at China’s ports fell below $100 for the first time in years.

June China iron ore futures contract (source: barchart.com)

And steel rebar futures on the Shanghai exchange are also continuing to fall. Some of these declines are of course related to declining construction activity.

June China steel rebar futures contract (source: barchart.com)

Once again, most economists do not expect a “hard landing” for PRC because the government has enormous resources to “backstop” the nation’s economy. Nevertheless, a number of indicators from China still point to persistent risks to growth.