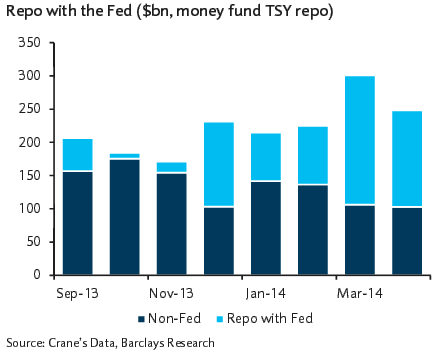

Some economists have raised concerns that the Fed’s experimental reverse repo program (RRP) could crowd out banks. The latest data from Barclays shows that as RRP expanded, money market funds have been placing a greater percentage of their overnight liquidity with the Fed rather than with banks.

Source: Barclays Research

Before the Fed’s program was launched, money market funds would have to go into the market daily to see where they can place their cash on a secured basis (take in securities as collateral). Given how awash the system is with liquidity these days, banks have had a fairly limited need for overnight funding from money funds. They would therefore offer near zero and sometimes negative rates, depending on how much liquidity money market funds wanted to park overnight. The process was stressful and competitive for these funds.

Now comes the Fed with a fixed rate offering – without the competitive pressures (although for a limited amount only). It’s not a surprise therefore that money market funds are using RRP to the fullest extent allowed. The question of course is what will happen when the Fed begins to offer unlimited amounts of this product – which is ultimately the goal. Will all of this overnight liquidity go to the Fed and will it create a funding problem for banks? The answer is: banks will be just fine.

To the extent banks are flooded with liquidity and don’t need this overnight capital from money market funds, a great deal of the funds’ cash will indeed go to the Fed. However if some banks decide to keep their funding source from money funds, they would simply need to offer a slightly higher rate. At some level money market funds will take on some bank risk (with collateral) in order to get a better rate than what the Fed is offering. RRP simply becomes the absolute floor on secured funding rates – funds would only use it if better rates are not available. There is no “crowding out” risk with RRP.