As anyone who has read our series on “Mario Draghi’s Monetary Nightmare” knows well, the biggest problem Europe faces is not inflation (or rather deflation according to its Keynesian voodoo priests)but loan creation: nearly 6 years after the Lehman collapse, the monetary transmission mechanism i.e., loan-funded growth in Europe continues to be abysmal, mostly due to lack of credit demand, which in turn means that any attempt by Draghi to unclog Europe’s monetary pipeline via NIRP, QE, or what have you, is set to fail. It also explains why the latest TLTRO expansion by the ECB (if it ever actually takes place of course: recall Europe’s OMT program still does not officially exist) has and will achieve nothing for the real economy but certainly has boosted carry trades into overdrive leading to record lows for all peripheral bond yields.

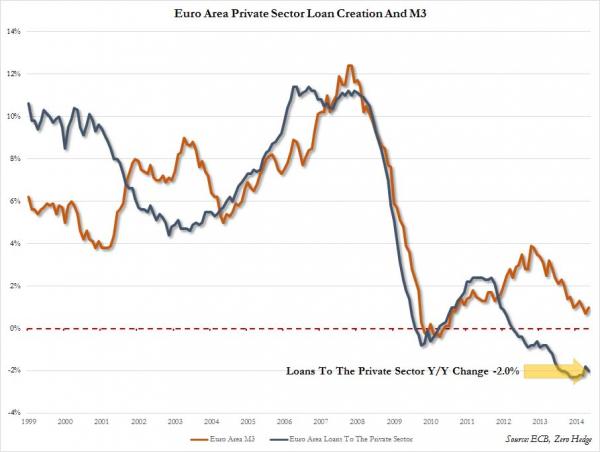

Alas, today’s ECB update on Monetary Developments in the Euro Area was as grim as always, with the all important series of Loans to the private sector sliding once again by 2.0% Y/Y, worse even than April’s -1.8% contraction, driven by a €43 billion collapse in loans to households. This happened even as the now largely meaningless M3 rose by 1.0%, an increase to April’s 0.7% Y/Y change.

In other words, Europe is in bad a shape as pretty much ever, and loan creation is just fractions above its all time low print of -2.3% from late 2013.

Â

Â

But that’s just part of the story, the part that we have long said will not change until there is dramatic debt destruction in Europe, and until the trillion or so in bad loans parked at Europe’s banks are somehow alleviated.

Where things get really messy is when one looks at the actual components of the contraction. As Goldman explains, “Euro area bank lending to non-financial corporations (NFCs) fell by €7.6bn in May, after a €6.3bn contraction in April. Lending rose in France and declined in Spain and Italy, while it was roughly unchanged in Germany. There was a significant decline in lending to households for house purchase related to sales and securitisation. Broad money growth rose from +0.7%yoy to +1.0%yoy, stronger than expected (Cons; +0.8%yoy).”