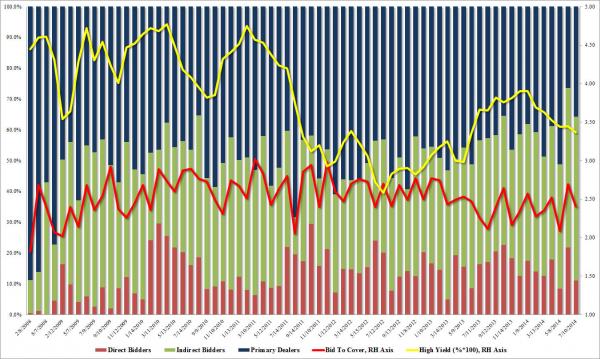

In what was practically a carbon copy of yesterday’s 10 Year auction, moments ago the Treasury sold $13 billion in 30 Year paper which priced at 3.369%, the lowest yield since June of 2013 when it hit 3.355, even if it meant a modest 0.9% bps bps tail to the 3.360% When Issued. The internals were both good and bad: bad in that the Bid To Cover came at 2.40, modestly lower than last month’s 2.69 but better than the TTM average of 2.38. Good in that the Indirect takedown of 53.25 was the highest since we began keeping records in 2008, and continues the trend seen last month in which Indirects bought more than half of the auction. This strength, however, was offset by a drop in the Direct bid by nearly half from last month’s 21.8% to 11.1%, leaving a modest 35.7% to the Dealers to promptly flip back to the monetizing Fed.

Curiously, while there barely a response to note of across the curve, the USDJPY promptly sprang up as if stung in a replica of yesterday’s reaction, which in turn managed to pull Spoos higher. If this is the kneejerk reaction programmed by algos into the their FX signals, the perhaps a bond failure will be just the catalyst to pushes equities limit up?

Â