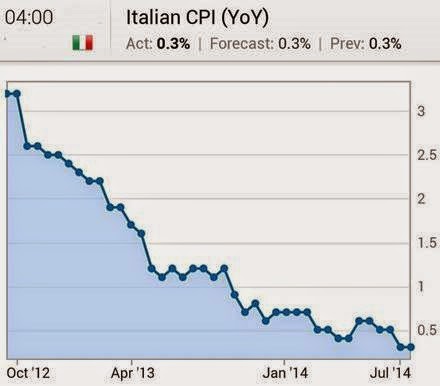

In spite of weakening economic growth, persistent credit contraction, and dangerously low inflation rate in a number of member states (chart below), the ECB continues to resist calls for Fed-style outright securities purchases. Instead the central bank is betting on the recently announced TLTRO program (see post).

Â

|

| Source: Investing.com |

The key reason for avoiding outright quantitative easing is, supposedly, the ECB’s fear of creating a moral hazard. With a ready buyer of government debt and low market rates, some member states would no longer focus on cutting deficits.

Natixis: – The ECB’s problem is that it does not want to create incentives for governments to refrain from correcting fiscal deficits or avoid improving their public finance situation. What is rejected by the ECB is the moral hazard that would result from the central bank buying government bonds.

Fair enough. But a recent report from Natixis argues that the combination of the TLTRO lending and the OMT backstop program creates conditions that are nearly identical to quantitative easing.

Any QE program aims to increase the monetary base (by raising banks’ excess reserves) and to push down longer term interest rates via securities purchases. As an extreme example of this, consider Japan’s massive QE effort (see post). Both objectives have been met: long-term rates are at ridiculously low levels (0.53% on 10-year JGBs) while the monetary base is at a record.

|

| Source: Investing.com, BOJ |

Similarly (though not to the same extent) the ECB’s programs will mimic QE without actually buying any government securities. Here is how:

1. Long term rates across the Eurozone are already at incredibly low levels. The ECB’s forward guidance, weak growth, and recent geopolitical risks have pushed German rates to new lows (see chart). On the other hand the OMT program, often called the “Draghi put”, has suppressed periphery yields. Furthermore, with short-term rates near zero and low capital requirements to hold sovereign bonds, the euro area banks have been loading up on this paper in a massive carry trade – pushing yields even lower.