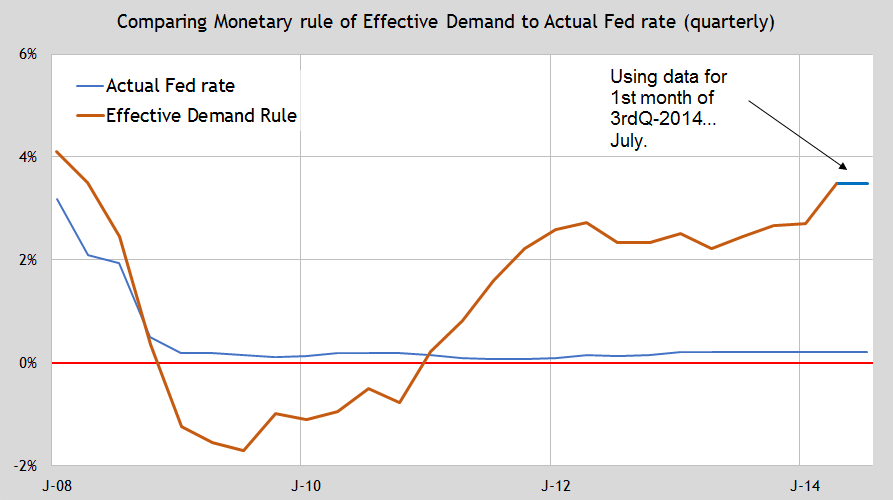

What would the Fed funds rate be as if we were in normal times? Basically, what would the Fed funds rate be if we used a rule instead of the discretionary policy being used by the Fed?

I use my Effective Demand rule using the CPI (less food & energy) data released just this morning. My ED rule has an advantage over other rules that use GDP numbers because they have to wait 3 months for the GDP numbers. I do not. So here is the monthly update of where the Fed’s base nominal interest rate would be as if we were in normal times…

The 3rd quarter of 2014 so far is starting out by reinforcing the jump up in the ED “rule†rate seen in 2nd quarter 2014. The ED rule is giving the same rate of 3.5% for July 2014. Let me show you how this is calculated.

Here is the Effective Demand rule…

Effective Demand Fed Rate Rule = z*(TFUR2 + LSA2) – (1 – z)*(TFUR + LSA) + inflation target + 1.5*(current inflation – inflation target)

z = (2*LSA + NR)/(2*(LSA2Â + LSA))

TFUR = Total Factor Utilization Rate, (capacity utilization * (1 – unemployment rate)), 74.3% for July 2014.

LSAÂ = Effective Labor Share Anchor is currently 74.5.

NRÂ = Natural real rate of interest is assumed to be 1.8% currently.)

Inflation target = 2.0%

Current inflation (CPI less food & energy)Â = 1.855% in July 2014.

1.5 coefficient = To give the Fed rate leverage when inflation gets off target. Fed rate would change 1.5x more than inflation is off target.

We first determine the z coefficient…

z = (2 * 74.5% + 1.8%)/(2*(74.5%2Â + 74.5%)) = 58.00%

Then we determine the TFUR for July 2014…

TFUR = 79.2% * (1 – 6.2%) = 74.3%

Now we use the Effective Demand rule to determine the base nominal rate…

58%*(74.3%2 + 74.5%2) – (1 – 58%)*(74.3% + 74.5%) + 2.0% + 1.5*(1.855 – 2.0%) = 3.5%

The ED rule worked very well for decades before the crisis. We get an idea of the twilight zone in which monetary policy now finds itself. The Fed just does not understand the unusual shift in Effective Demand which has occurred in the last decade.