by Jens H.E. Christensen and Simon Kwan – FRBSF Economic Letter, Federal Reserve Bank of San Francisco

An ongoing concern has been that the public might misconstrue the Fed’s forward guidance about future monetary policy and underappreciate the extent to which short-term interest rates may vary with future news about the economy. Evidence based on surveys, market expectations, and model estimates show that the public seems to expect a more accommodative policy than Federal Open Market Committee participants. The public also may be less uncertain about these forecasts than policymakers.

Â

Recently, subdued levels of volatility in financial markets have received some attention. For example, Federal Reserve Chair Janet Yellen (2014) noted that “indicators of expected volatility in some asset markets have fallen to low levels, suggesting that some investors may underappreciate the potential for losses and volatility going forward.†Prices of financial assets, such as stocks and bonds, are sensitive to unexpected changes in interest rates because their present values are determined by discounting future cash flows. Thus, the low volatility in asset markets could, in part, reflect market participants’ relative certainty about the future course of interest rates.

In this Letter, we assess the private sector’s views about future monetary policy in terms of both expected levels of the short-term interest rate and the uncertainty or disagreement in those expectations. Through its “forward guidance,†the Federal Reserve’s policymaking body, the Federal Open Market Committee (FOMC), provides an indication to the public about the stance of monetary policy expected to prevail in the future. Furthermore, since 2012, the FOMC participants’ projections of the appropriate target for the federal funds rate over the next several years and in the longer run have been included as part of their quarterly economic projections, which are released to the public. Research has shown that this communication of interest rate projections can better align the public’s and the central bank’s expectations, which could lead to improved macroeconomic performance (see, for example, Rudebusch and Williams 2008). However, an important concern is that the public might not give enough weight to how dependent the central bank’s guidance is on both current and incoming data. Thus, the public could underestimate the conditionality and uncertainty of interest rate projections.

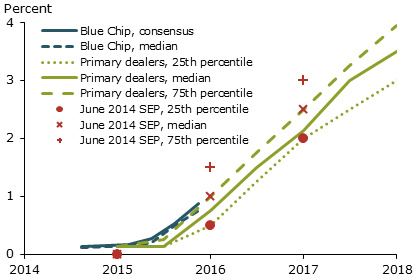

We assess the public’s expectations about future monetary policy from three sources: (1) surveys of economic forecasters and primary dealers, (2) market prices of federal funds and Eurodollar futures, and (3) estimates from a financial-econometric model. We then compare these public expectations with the expectations reported in the June FOMC participants’ federal funds rate projections (Board of Governors 2014). Our analysis shows that, on balance, the public seems to expect more accommodative policy than FOMC participants. One measure of uncertainty also shows the range of the public’s forecasts is somewhat smaller than that among FOMC participants, suggesting the public also may be less uncertain about their projections.