Abenomics Keeps Sputtering – What To Do?

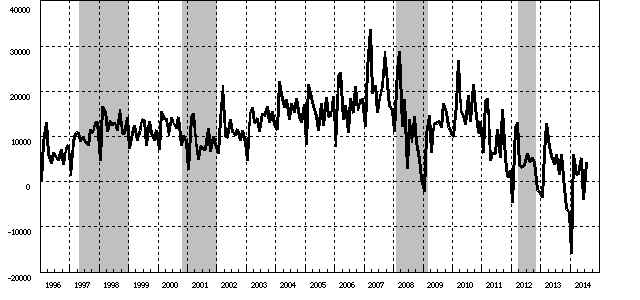

We have frequently discussed the nonsensical attempt by Japanese prime minister Shinzo Abe and BoJ governor Haruhiko Kuroda to print and spend Japan back to prosperity in these pages. By now it is well known that devaluing the yen has not achieved the desired effect, but rather the opposite. Not only have exports not really received the expected boost, but Japan’s trade and current account surplus have decreased markedly, even posting negative numbers for the first time in decades. Of course, currency debasement never works: it cannot work.

Japan’s current account over the past two decades.

We would like to point out though that a trade or current account surplus is not a measure of a country’s prosperity anyway. So even if the devaluation gambit had “succeededâ€, its success would have been meaningless and any positive effects would have been strictly transitory. Japan’s consumers would have suffered just as they are suffering now. As Ludwig von Mises stated with regard to alleged advantages of devaluation:

“The much talked about advantages which devaluation secures in foreign trade and tourism, are entirely due to the fact that the adjustment of domestic prices and wage rates to the state of affairs created by devaluation requires some time. As long as this adjustment process is not yet completed, exporting is encouraged and importing is discouraged. However, this merely means that in this interval the citizens of the devaluating country are getting less for what they are selling abroad and paying more for what they are buying abroad; concomitantly they must restrict their consumption. This effect may appear as a boon in the opinion of those for whom the balance of trade is the yardstick of a nation’s welfare.

In plain language it is to be described in this way: The British citizen must export more British goods in order to buy that quantity of tea which he received before the devaluation for a smaller quantity of exported British goods.â€

In short, devaluation means securing a strictly temporary advantage for a small sector of the economy – export-oriented companies – while impoverishing all consumers concurrently. In the end, not even the advantages for exporters will be maintained, as domestic prices will inevitable adjust. As strategies for economic revival go, this has to be one of the most moronic ones ever devised. Not surprisingly, the EU’s coterie of economic planners is also fervently in favor of debasing the euro. Especially France’s government has been quite vocal in this respect, which is telling. The situation in the EU at present is this: the ECB has taken the advice of the biggest economic illiterates in political power in the EU.