If yesterday the bombardment, no pun intended, of bad news from around the globe was too much even for Mahwah’s vacuum tubes to spin as bullish - for stocks – news, then tonight’s macro economic updates have so far been hardly as bombastic, with the only real news of the day has Germany’s Ifo Business Climate reading, which dropped from 106.3 to 105.8, declining for the 5th month in a row, missing expectations, and printing at the lowest level of since April 2013! (More from Goldman below) Net result: Bunds yields were once again pushed in the sub-1% category, even if stocks today are higher because the European data is “so bad it means the ECB has no choice but to do (public instead of just private) QE” blah blah blah.

Goldman on the Ifo:

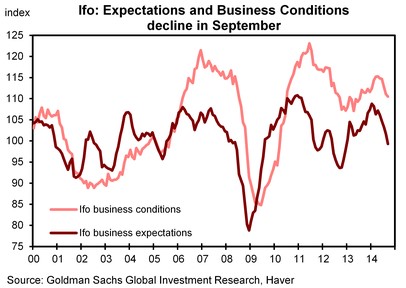

Bottom line: The Ifo index declined more than expected in September. The decline is in contrast to yesterday’s marginal increase in the September German Composite PMI, pointing to some uncertainty about the underlying trend of the German economy.

The Ifo index declined to a level of 104.7.0 in September against expectations of a small easing to 105.8. The ‘assessment of current conditions’ edged lower to 110.5 after 111.1, while ‘expectations’ declined to 99.3 after 101.7. The decline in sentiment was broad-based, with all major sub-indices of the survey showing a lower reading in September.

Today’s Ifo figure stands in contrast to the stabilization of the composite PMI, which on the flash reading printed at 54.0 in September after 53.7.

Â

Â

Expect USDJPY momentum ignition to go berserk any minute as the HFTs wake up and are ordered by central banks to send futures higher, and the USDJPY 109 tractor beam to support the broader “market”, especially if today’s new home sales is as bad as we (and Goldman’s former head of housing research) think it may be: because the time to start pricing in the untaper has almost arrived.

Asian investors are more on the front foot overnight as key equity markets rebounded from their previous day’s losses. Chinese equities extended their run higher overnight with the HSCEI and Shanghai Composite up +1.0% and +0.8% following the slight beat in China’s flash PMI headline yesterday. Markets are also seemingly overlooking another corporate default story in China. Chinese steel transporter Anhui Wanjiang Logistics said RMB2bn of its loans were overdue and that its chairman had been detained by police. The company has about RMB16.7bn in debt and is said to have used up its credit quota leaving it with no working capital (Reuters). Staying on China, S&P has said overnight that widespread defaults by local government financing vehicles are unlikely in the next year or so as they have sufficient resources (ie to cut non-core spending, improve revenue collection or make asset sales) to absorb weaker property related revenue (which accounted for about 20% of local government revenues in 2013). Away from China we are seeing modest gains across Taiwan and Korea although Japan has reopened after hols with a softer tone. Australian equities are lagging the rest not helped by a rather bleak commodity price projection by the Bureau of Resources and Energy Economics with broadly flat Iron ore and lower thermal coal prices in 2015.

Asian stocks little changed with CSI 300 outperforming and the ASX 200 underperforming. MSCI Asia Pacific little changed to 143.2. Nikkei 225 down 0.2%, Hang Seng up 0.4%, Kospi up 0.3%, Shanghai Composite up 1.5%, ASX down 0.7%, Sensex down 0.1%. 6 out of 10 sectors rise with utilities, energy outperforming and telecom, information technology underperforming.

European equities languish around yesterday’s lows with initial commodity-inspired support faltering as markets head into the US session. Initial positive sentiment has eroded with European participants provided with a lack of further catalysts to the upside, with the mixed German IFO report (business climate 104.7 vs. Exp. 105.8) revealing a 5th monthly consecutive decline for the headline figure adding to the recent negativity. In terms of stock specific news Pfizer PFE is said to be undeterred by Treasury restriction inversions and are weighing options including AstraZeneca bid. Elsewhere, Dutch courier TNT (-11%) is the underperformer in Europe after issuing a profit warning amid a deterioration in European trading conditions. 7 out of 19 Stoxx 600 sectors rise; basic resources, telecom outperform while media, banks underperform. 26.2% of Stoxx 600 members gain, 69% decline. Eurostoxx 50 -0.1%, FTSE 100 -0.2%, CAC 40 little changed, DAX -0.2%, IBEX -0.9%, FTSEMIB -0.1%, SMI +0%