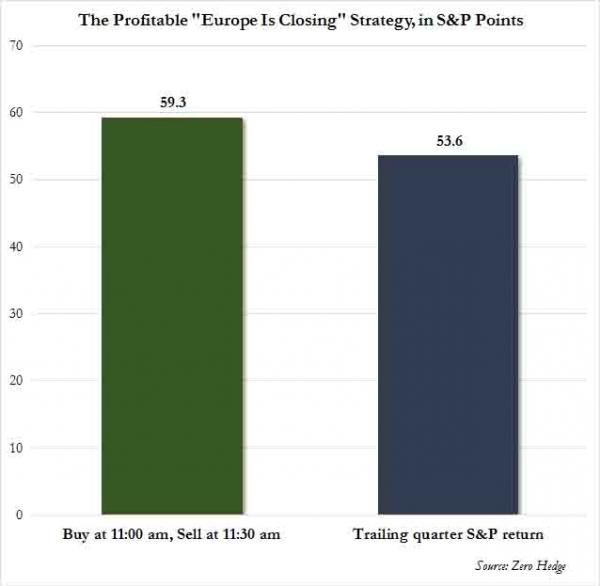

The relentless regurgitation of the only two rumors that have moved markets this week, namely the Japanese sales tax delay and the “surprise” cabinet snap elections, was once again all over the newswires last night in yet another iteration, and as a result the headline scanning algos took the Nikkei another 1.1% higher to nearly 17,400 which means at this rate the Nikkei will surpass the Dow Jones by the end of the week helped by further reports that Japan will reveal more stimulus measures on November 19, although with US equity futures rising another 7 points overnight and now just shy of 2050 which happens to be Goldman’s revised year-end target, the US will hardly complain. And speaking of stimulus, the reason European equities are drifting higher following the latest ECB professional forecast release which saw the panel slash their GDP and inflation forecasts  for the entire period from 2014 to 2016. In other words bad news most certainly continues to be good news for stocks, which in the US are about to hit another record high, with the bulk of the upside action once again concentrated between 11:00 and 11:30am.

Those looking for bad economic news got another boost out of China which reported an across the board miss last night when it announced that October’s Fixed Assets Investments (+15.9% YTD yoy v +16.0% expected) and Retail Sales (+11.5% yoy v +11.6% expected) both missed but Industrial Production (+7.7% yoy v +8.0% expected) was a quite notable miss and immediately spun as bullish for even more PBOC intervention, which however continues to be in the form of direct liquidity injections, this time into small banks.

So with global growth continuing to founder, oil prices not unexpectedly dipped lower once more with Brent dropping further below $80, or $79.56 at last check, with WTI the usual $3 or so below, and making life for US shale companies increasingly more difficult. Them, and oil exporting nations too, after the Ruble once again dipped by 1% overnight but it was the Nigerian Naira which tumbled once again to fresh record lows, as the oil-exporting nation pain hits a crescendo.

European equities languish firmly in the green in a continuation of the price action seen overnight, whereby Japanese equities saw further upside from continued expectations of a sales-tax delay and possible snap election. Furthermore, European equities continue to drift higher following the latest ECB professional forecast release which saw the panel slash their GDP and inflation forecasts for 2014/15/16, which has helped hammered home the point that further stimulus may be warranted in the Eurozone. On a sector specific basis, utilities are the sole underperformers in the European equity sphere following a less than impressive pre-market report from RWE (-2.6%). The strength in stocks subsequently supressed some of the price action in fixed income markets, with Gilts holding tight following their sizeable gains yesterday. However, heading into the North American open, fixed income products have begun to tick higher following the ECB forecasts and their potential implications for the future path of ECB policy

Looking at the rest of the day ahead, today we will get the JOLTS report in the US, which while delayed by a month remains one of Yellen’s favorite economic indicators. In terms of what to expect from the JOLTs release today, in order for Yellen to be comfortable that the labour market has returned to more of a normalized state, the hiring and quits rates each need to improve several tenths from their current readings (3.3% and 1.8% respectively). We also have the initial jobless claims print and October budget statement. Fed member Plossner will also be speaking today. In Europe ECB’s Lautenschlaeger will be speaking this morning and we are expecting Coeure to speak this afternoon in New York so will keep an eye open for any interesting developments there.