Chalk up another €5 billion in capital flight from Greece in April. Total eurozone exposure to Greek currency liabilities now sits at €115 Billion, not counting accelerated capital flight in recent weeks.

The following two charts produced with data from EuroCrisis Monitor.Â

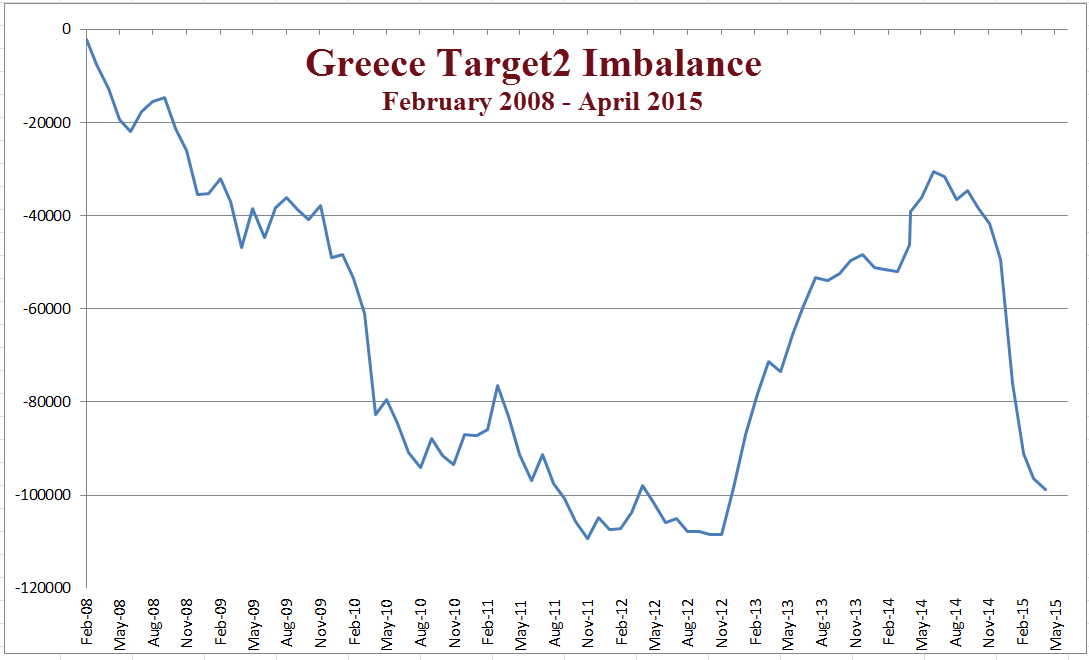

Greece Target2 Imbalance Since February 2008

Greece Target2 Imbalance Detail Since June 2014

The chart shows a rise of €2 billion but that does not count cash.

Target2 ExplanationÂ

For a refresher course on Target2, please see Reader From Europe Asks “Can You Please Explain Target2?”

Intra-Eurosystem Liabilities Â

The latest Intra-Eurosystem Liabilities from the Bank of Greece are €114.95 billion as shown below.

Change From Last Month

Last month, eurozone exposure to Greek liabilities was €96.427 billion of Target2 imbalances plus another €14.028 billion net liabilities related to the allocation of euro banknotes.

“The past week in May was more challenging compared to the previous ones in the month, with daily outflows of 200 to 300 million euros in the last few days,” a senior Greek banker said yesterday.

In the last week alone, it seems likely another €2 billion was pulled from Greek banks. The total May drain will not be reported until June 10.

The ECB is attempting to stem the flow by not upping emergency liquidity assistance (ELA) as noted yesterday in Run on Greek Banks Accelerates; ECB Halts Emergency Funding Hike; Untangling the LiesÂ

Everyone Prepared?Â

When the ECB and Germany say they are prepared for Grexit, do they include taxpayers who will have to foot the bill for default?

My friend Lars from Norway pinged me with this observation today…Â

Greek GDP is about €180 billion. Public sector is 60% of the total. That makes the private sector contribution to GDP about €72 billion.

Total public sector debt is close to €500 billion (not €320 billion as quoted by the mainstream media). So a private sector with €72 billion final sales will have to service a debt load of €500 billion.

Isn’t the conclusion obvious?

Regards

Lars