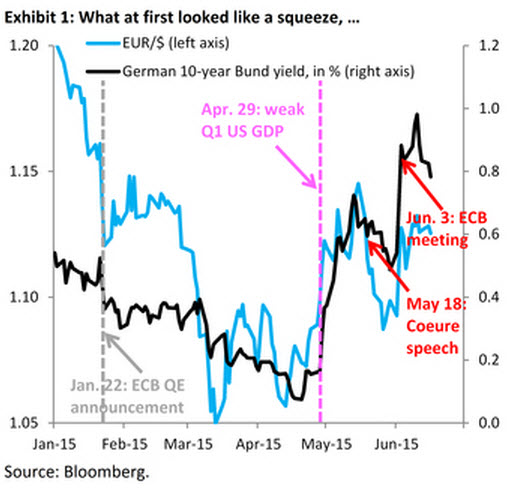

When the sell-off in German Bunds first got going, it looked like a temporary squeeze, with the largest position in the market – the ECB QE trade – coming under pressure after much weaker-than-expected Q1 GDP on 4/29.

Â

However, as (Draghi mouthpiece) Goldman notes, there is something more than supply dynamics or ECB communications going on, as the Bundesbank (Buba) buying has fallen short of its purchases (in average maturity terms) from the very beginning. Goldman warns, ominously, this kind of signal – from the key hawk in the Eurosystem – has the potential to undercut the credibility of ECB QE, since it weakens the portfolio balance channel.

*Â *Â *

Goldman previously argued that the weak activity reading rattled a market that had been operating on a core thesis of strong US growth. The resulting uncertainty caused Bund yields and EUR/$ to rise, with the DAX also selling off on the day. Since then, something more ominous has come into play…

One clue has been the communications ping pong from the ECB. On May 18, Executive Board member Coeure said “the rapidity of the reversal in Bund yields is worrisome,†citing it as another example of “extreme volatility in global capital markets.â€

ECB President Draghi sent the opposite message on Jun. 3, saying “one lesson is that we should get used to periods of higher volatility,†followed on Jun. 10 by Executive Board member Coeure stating that “the ECB does not intend to counter [Bund] volatility in the short term.”

Goldman took a dim view of all this in our last FX Views, even if a charitable interpretation is that President Draghi basically sent a dovish message on Jun.10 and simply didn’t want to signal “activism” in the face of short-term volatility.

After all, one goal of ECB QE ought to be to make Europe’s safe haven asset (Bunds) expensive, so that investors get pushed into risky assets like equities and the Euro periphery.

If there is ambivalence, it sends a harmful message to markets that, after all, are still new to ECB QE. This might be one reason why EUR/$ has held up, even as US data (payrolls, retail sales) have picked up.

Â

There is something more than supply dynamics or ECB communications going on, something that has the potential to undercut the credibility of ECB QE.

As Goldman explains below, the Bundesbank has reduced the weighted-average maturity of its Bund purchases from 8.1 years in March to 5.7 in May, in contrast to the Eurosystem as a whole where this number has stayed around 8.0 years.