Following quarters of declining investment bank revenue from sales and trading even at such Fed-backstopped hedge funds as Goldman Sachs, and especially the one-time golden goose, FICC, we hardly need to explain that over the past several years, whether or not due to declining liquidity, total trading turnover/volume and thus commissions, especially in high-margin, OTC products has plunged.

Where has it plunged the most?

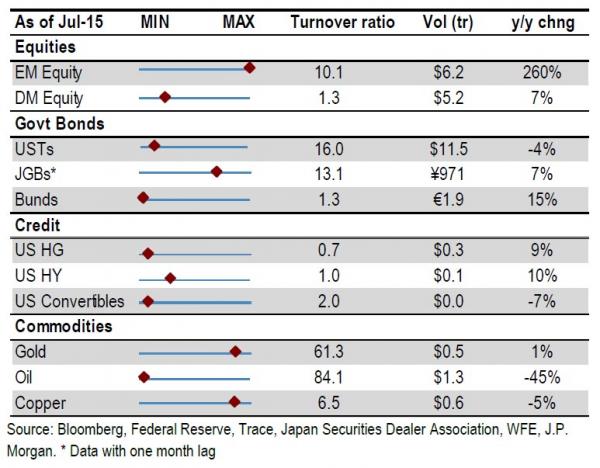

To answer that question, which in retrospect may appear trick in nature since it is more or less “all”, we go to the latest Trading Turnover Monitor from JPMorgan which looks at the total Turnover ratio (i.e. the ratio of monthly trading volumes annualized divided by the outstanding amount), for all key asset classes, equities, government bonds, credit and commodities, with a Min-Max range going back to January 2005, and find that with the exception of gold, where turnover in the past 3 months has soared, excluding the “Asian” assets, i.e., EM equities (think China, which incidentally is the asset class that saved bank Q2 earnings; the volume surge won’t be repeated in Q3) and Japan bonds (most of which due to the BOJ’s open monetization almost daily), the turnover ratio virtually across the board is non-existent and is the lowest it has been in the past decade!

Indeed, as the chart below shows, from oil to bunds, to US HG and Convertible debt, to USTs and even to Developed Market stocks, turnovers are virtually non-existent, while the only place where there has been a transitory surge in turnover has something to do with Chinese stocks, where volume however has been quite muted in recent months ever since the bubble died.

The take home message from the above is simple: anyone hoping for a rebound in trading volumes… don’t.

And since the bank stock rebound over the past few months is still completely inexplicable to anyone who is not a lobotomized momo, perhaps somehow in the past 2-3 years, the complete collapse of Net Interest Margin to record lows (and soon to be inverted) was spun, alongside with a Fed hiking rates and tightening financial conditions, as bullish. We don’t know.