The Fed is going to raise rates next month…and kill the REIT sector.

At least that’s the received wisdom. The problem is, it isn’t true. Or at the very least, it isn’t supported by history.

We’ll start with the first assumption: That the Fed will raise rates. Recent comments by Janet Yellen and her peers on the Federal Reserve Board suggest that the Fed will indeed raise the targeted Fed funds rate next month. Or if not next month, then almost certainly by December.

But it’s hard to see the Fed raising rates by more than 0.25% – 0.50% unless we see the pace of economic growth suddenly step it up a notch. The dollar is already strong enough to stifle export growth, and the Fed isn’t looking to make a bad situation worse. So again, unless something radically changes, this will be the mildest tightening cycle in modern history.

But let’s play devil’s advocate here and assume, for the sake of argument, that this tightening cycles looks like the last several before it. It’s still pretty ambiguous as to what effect that would have on REIT prices.

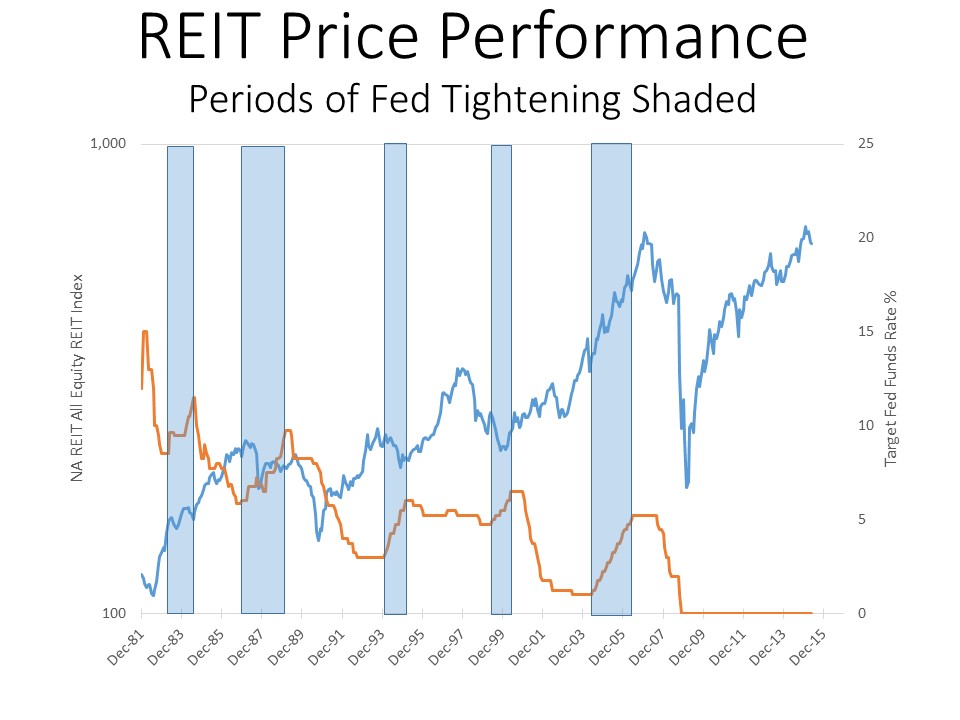

The chart below tracks the price performance of the NAREIT All Equity REIT Index going back to the early 1980s and compares it to the Federal Reserve’s targeted Fed funds rate. Periods of extended tightening are highlighted in blue.

Â

We’ve had five periods of extended tightening since 1981. In three of them, REIT prices did indeed suffer. But in the other two — and keep in mind, that is fully 40% of the total — REIT prices actually did very well. In fact, the tightening cycle of the mid-2000s coincided with one of the greatest bull markets in the history of REITs as an asset class.

And let’s not forget that this is the most telegraphed Fed tightening in history. Yellen has been preparing us for this day formonths. And as a result, income-focused like REITs have had a terrible year, basically pricing in the Fed tightening months in advance. After topping out at $89.27 per share in late January, the Vanguard REIT ETF (VNQ) fell to as low as $74.67 by late June. That’s a decline of 16% based almost exclusively on Fed fears.