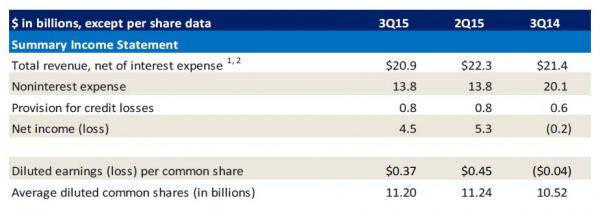

While yesterday’s JPM results missed from the top to the bottom, coupled with a surprising and aggressive deleveraging of the bank’s balance sheet which has shrunk by over $150 billion in 2015 mostly on the back of a decline in deposits, Bank of America reported numbers which were largely the opposite when it printed a modest beat on both the top line with $20.9 billion in revenues (adjusted sales of $20.6Bn vs Exp. $20.5Bn), down $500 million from a year ago, and the bottom line: generating $0.35 in adjusted earnings in the quarter, 2 cents better than the $0.33 consensus estimate.

Â

As shown in the chart above, the company’s official EPS was $0.37 but this contained the following adjustments:

- ($0.03) per share after-tax from negative market-related NII adjustments 1 ($0.6B pre-tax)

- $0.02 per share after-tax from positive net debit valuation adjustments ($0.3B pre-tax)

- $0.02 per share after-tax net positive impact from gain on sales of consumer real estate loans ($0.4B pre-tax), chargefor UK payment protection insurance ($0.3B pre-tax), and income tax benefits related to certain non-U.S. subsidiaryrestructurings

As to where that all important 2 “beating” cents came from, why the usual place of course:

“The net reserve release was $126 million in the third quarter of 2015, compared to a net reserve release of $407 million in the third quarter of 2014.”

Which is odd considering this takes place in a quarter when everyone else (coughjefferiescough) is provisioning for deep credit losses.

The reason for the improvement on the expense side was cost-control, with total noninterest expenses flat at $12.7 billion, while LAS and litigation were a modest $1.1 billion. Also worth noting: BofA continue to layoff workers, which dropped from 230K a year ago to 215K in Q3, down 2K from the previous quarter. Goldman Sachs continues to be the only bank in the US which is hiring bankers.

Â

In any event, the number was “good enough” because as a reminder, it was a year ago that BofA posted a surprising loss on the back of massive legal charges. And as we wroted previously, due to the swing from a loss to a profit, far more than AAPL, BofA would be the single biggest earnings swing factor in Q3 not only for the financial sector but also for the S&P as BofA alone will contribute to about 1.4% of the Y/Y change in S&P earnings!