This week’s report is going to deviate a little from the norm as I am just going to focus on the technical impact from the Brexit vote on Thursday, and the subsequent fallout on Friday.

First, let’s pick up with where I left off on Tuesday:

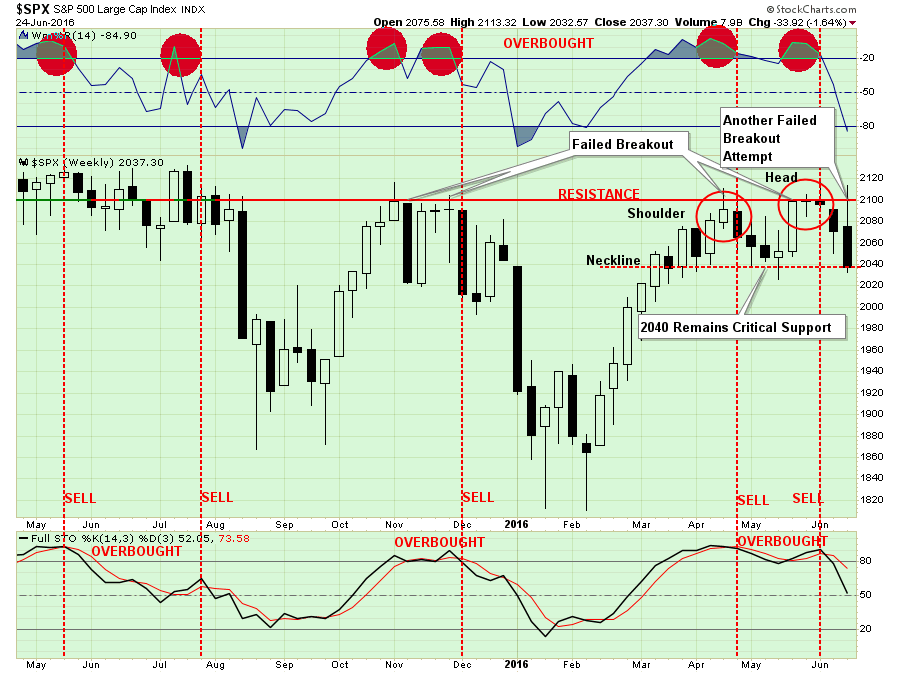

The market has repeatedly made attempts to break out above 2100. But that level has rejected investors more often than Josh Richardson at the net. (Miami Heat)

The good news, if you want to call it that, is that 2040 still contains the downside to the market currently. However, the neckline forming at 2040, on a weekly basis, will become critically more important if the development of a “head and shoulderâ€Â formation comes to fruition.Â

As has been the case since the beginning of the year, the markets have migrated investment strategies to follow “Fed Speakâ€Â and headline events rather than fundamentals. The annotated chart below is rapidly running out of room to notate these events while earnings continue to deteriorate.

“Of course, the market ignoring fundamentals and focusing on “Fed Speak†is not a new innovation but something seen at the peak of the last two major bull markets.â€

As I have stated repeatedly over the last several weeks, with risk outweighing reward, a more cautious stance to portfolio management should be considered. It is always why I continue to hold excess levels of cash:

“However, if the holding of cash is a ‘tactical’ holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.â€

The chart below shows the now 13-month long sideways trading range of the market. However, most importantly, the downward trending price pattern remains in place. The recent failure at the downtrend resistance line remains a concern as well as the violation of the short-term moving average which has been acting as support.Â

The vertical blue-dashed lines denote market sell signals where subsequent price action has been poor, to say the least. While a “sell signalâ€Â is NOT CURRENTLY in place, it will not require much further deterioration in price to trigger one.

Again, as noted above, the compression that was building between the short-term moving average (blue dashed line) and the current “downtrend resistanceâ€Â was due to resolve itself. The break to the downside puts 2040 support, as noted above, into focus.

The problem for investors remains the focus on short-term “hopesâ€Â rather than longer-term fundamental dynamics. The issue of such “short-termismâ€Â is such a focus has had generally poor longer-term outcomes. As discussed in the “Theory Of Bubblesâ€:

“History is replete with market crashes that occurred just as the mainstream belief made heretics out of anyone who dared to contradict the bullish bias.

It is critically important to remain as theoretically sound as possible. The problem for most investors is their portfolios are based on a foundation of false ideologies. The problem is when reality collides with widespread fantasy.â€

DO NOTHING

Last Tuesday, while the markets were ramping higher on expectations Britain would “remain†in the Eurozone, I wrote:

“There are times in portfolio management where ‘doing nothing’ is better than“doing something.â€Â This is one of those times.

With portfolios already running at just 50% of total recommended equity exposure, portfolio risk is already substantially mitigated. This leaves us is the best place to be for the moment as we await the outcome of the ‘Brexit’ vote on Thursday and the culmination of Yellen’s testimony on the ‘Hill.’

From that vantage point, we can then assess the markets and make a reasonable assumption about what to do next. Could we miss a bit of upside? Absolutely. But such a small lag is a much better outcome than trying to recoup a substantial loss if things go wrong.â€

Well, things certainly went wrong.

However, the problem is we remain trapped in limbo. With the markets holding above supports, but still within an overall corrective topping process, there is no reason to become extremely negative on the markets at the moment OR be extremely bullish.

In other words, the only option is to continue to “do nothingâ€Â until the market resolves its current state in one direction or another.Â

The bad news is the longer the market remains in this current state, the risk are rising of a more substantial downside break.

The chart below is a monthly chart of the S&P 500 with GAAP earnings and Peak Earnings shown. The current topping process, stuck below “all-timeâ€Â highs, is not too dissimilar to what has been seen at previous major bull market peaks. As was the case then, “doing nothingâ€Â may be the best solution.Â

BACK TO FUNDAMENTALS

While the initial shake out of the markets was severe, the “shockâ€Â of the exit will be quickly absorbed by the financial markets. In the longer-term, the markets will have to come back to focus on the fundamentals, which are, to say the least, wanting.

As Andrew Lapthorne noted from SocGen earlier this week (via ZeroHedge):

“Whatever the outcome of the Brexit vote this week investors will still be facing the prospect of negative rates and negative yields on a huge range of bonds, massive corporate leverage with worryingly rising delinquencies and of course expensive equity markets and falling profits. To that extent, these political events are a distraction from the main event, weak global economic growth and perverse asset markets. So whilst the market preference for the status quo might be celebrated in the short-term, actually when the fog clears all of the problems will still be there.“

He is absolutely correct. However, this note from Nomura on Friday reiterated the point: