Over three years ago we wrote “At $72.8 Trillion, Presenting The Bank With The Biggest Derivative Exposure In The World” in which we introduced a bank few until then had imagined was the riskiest in the world.

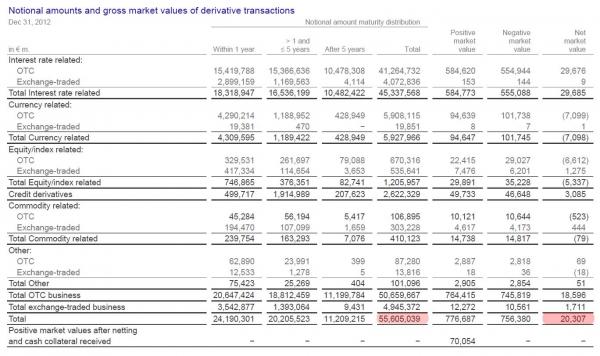

As we explained then “the bank with the single largest derivative exposure is not located in the US at all, but in the heart of Europe, and its name, as some may have guessed by now, is Deutsche Bank. The amount in question? €55,605,039,000,000. Which, converted into USD at the current EUR/USD exchange rate amounts to $72,842,601,090,000…. Or roughly $2 trillion more than JPMorgan’s.”

So here we are three years later, when not only did Deutsche Bank just flunk the Fed’s stress test for the second year in a row, but moments ago in a far more damning analysis, none other than the IMF disclosed that Deutsche Bank poses the greatest systemic risk to the global financial system, explicitly stating that the German bank “appears to be the most important net contributor to systemic risks.”

Yes, the same bank whose stock price hit a record low just two days ago.

Here is the key section in the report:

Domestically, the largest German banks and insurance companies are highly interconnected. The highest degree of interconnectedness can be found between Allianz, Munich Re, Hannover Re, Deutsche Bank, Commerzbank and Aareal bank, with Allianz being the largest contributor to systemic risks among the publicly-traded German financials. Both Deutsche Bank and Commerzbank are the source of outward spillovers to most other publicly-listed banks and insurers. Given the likelihood of distress spillovers between banks and life insurers, close monitoring and continued systemic risk analysis by authorities is warranted.

Among the G-SIBs, Deutsche Bank appears to be the most important net contributor to systemic risks, followed by HSBC and Credit Suisse. In turn, Commerzbank, while an important player in Germany, does not appear to be a contributor to systemic risks globally. In general, Commerzbank tends to be the recipient of inward spillover from U.S. and European G-SIBs. The relative importance of Deutsche Bank underscores the importance of risk management, intense supervision of G-SIBs and the close monitoring of their cross-border exposures, as well as rapidly completing capacity to implement the new resolution regime.