Greetings,

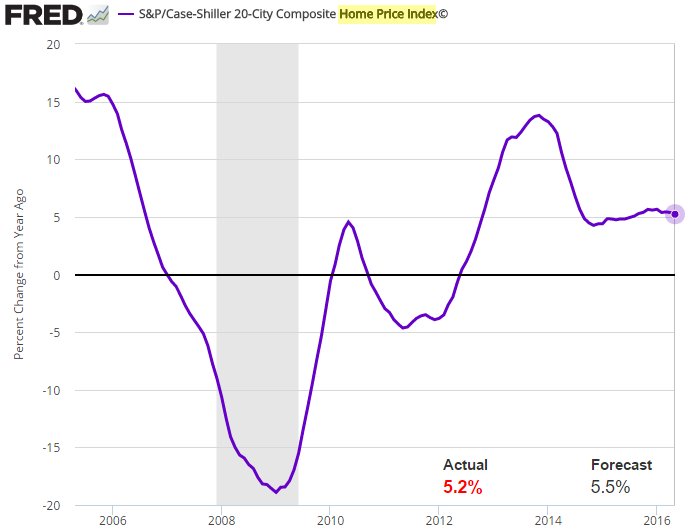

1. We begin with the United States where house price inflation eased somewhat but remains above 5% per year. As discussed before, with wages growing at roughly half that rate, housing appreciation needs to slow further to be on a sustainable path.

2. US new home sales rose to an 8-year high in June, materially beating consensus.

New home sales growth was uneven, with a big spike occurring in the $400k-$500k price range.

3. Shares of US homebuilders outperformed over the past couple of weeks on tight housing inventories (as discussed yesterday).

Source: Ycharts.com

4. The US services PMI from Markit was disappointing – here is a summary.

Source: @MarkitEconomics

5. The Conference Board US consumer confidence index was virtually unchanged from the prior month, with no visible impact from Brexit.

6. US consumer labor market sentiment improved in July. A rate hike could come as early as September if the Fed sees Brexit having only a limited impact on the US economy.

Source:  â€@jbjakobsen

7. The Philly Fed non-manufacturing survey shows a pickup in new orders while hiring moderates.

Â

Â

8. The Richmond Fed manufacturing report also shows a pickup in new orders and much tighter inventories.

Source: â€Richmond Fed ​

9. Broadly, while this US recovery is extremely slow, it has also been a relatively long one. As a result, the current GDP trajectory is now ahead of the 2001 recovery, which by this time was already in contraction mode.

Source: @Alan_Krueger

1. Switching to the Eurozone, the ECB (Eurosystem) consolidated balance sheet hits a new record (almost €3.3 trillion).

Source: ECB

Related to the above, the Eurozone monetary base now exceeds €2 trillion. A great deal of these balances is held at negative rates in the ECB Deposit Facility.

Source: ECB

2. Belgian business sentiment exceeds estimates. So far the Eurozone shows little sign of a broad negative impact from Brexit.

3. Negative yields in the Eurozone are increasingly showing up in corporate bonds. Some investment grade bonds are even yielding less than -40bp (the ECB’s cutoff rate).

In some ways, this could be viewed as “helicopter money” because by buying corporate debt and pushing yields into negative territory the central bank allows firms to make money in their interest expense account.