In his recent  testimony to the House of Commons in Ottawa, Governor Stephen Poloz stated  that “ our best plan right now, we think, is to wait for the next 18 months or soâ€. Immediately, investors interpreted this to mean that the Bank of Canada (BoC) would not make any decision to cut the bank rate prior to 2018. Upon clarification, the Governor said this waiting period was in reference to the time frame needed to close the output gap, not in reference to monetary policy changes. The confusion stems from a recent statement by the Governor that the BoC “actively†considered a rate cut in its October meeting , but decided to hold the key interest rate unchanged at 0.5 per cent.Â

However, the output gap and monetary policy are inextricably connected, even though the Governor did not mean to connect the two in his statements.

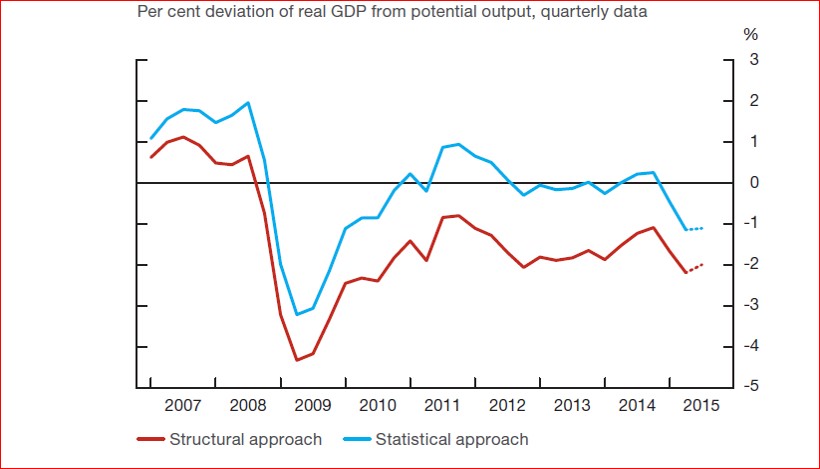

The output gap is a measure of excess productive capacity, a measure the BoC watches very closely to guide its policy deliberations. As Chart 1 demonstrates, the BoC uses two measures to calibrate capacity utilization. Although the measures are technically different, they tend to move in tandem and in the same direction .Canada ‘s output gap is in the range of 1.5-2.0 percent .

Chart 1 Estimates of Capacity Utilization

Source: Bank of Canada, October 2016 MPRÂ

This gap is sizable, especially in view of recent history. The Canadian economy has been operating at much less than full capacity— in terms of labour and capital utilization — for all the period since the 2008 financial crash. Moreover, successive years of underperformance results in a weaker economy as all resources continue to be underutilized.This has actually reduced the nation’s potential for growth. Each year that we underperform results in lower investment and employment growth in future years which, in turn, lowers potential growth. Â

As the BoC put it in its recent Monthly Policy Report (MPR) “declines in investment ….imply that, in the near term, potential output growth is more likely to be in the lower range of estimates†compared to prior years’ calculations. The decline in the growth rates can be traced to the decline in investment , principally, in the natural resource sector .However, the non-energy sector has failed to pick up that slack and, as a result, export growth has been missing in action.