This daily digest focuses on Yuan rates, major Chinese economic data, market sentiment, new developments in China’s foreign exchange policies, changes in financial market regulations, as well as market news typically available only in Chinese-language sources.

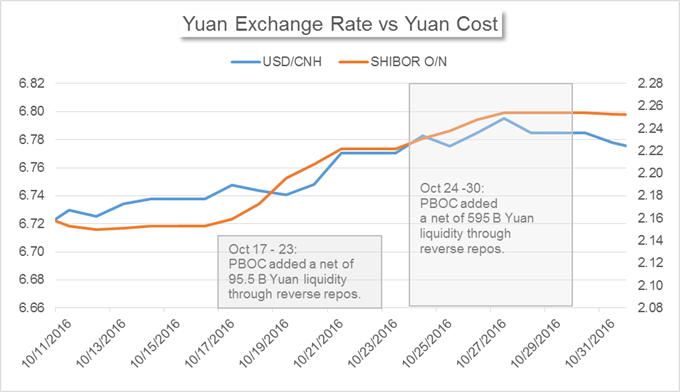

– Inconsistent moves between onshore Yuan liquidity injections and Yuan costs are likely driven by exchange rates.

- CICC forecasts that home sales in tier-one and tier-two cities will drop -20% in the fourth quarter.

- The housing prices in 30 Chinese cities in a survey fell -8% in October from the month prior.

Yuan Rates

– The PBOC sold 30 billion Yuan of 7-day reverse repos, 20 billion Yuan of 14-day reverse repos and 20 billion Yuan of 28-day reverse repos on Thursday. After deducting the 165 billion Yuan reverse repos matured on the day, the net liquidity reduced through reverse repos was 95 billion Yuan, the second withdrawal in a row.

Despite the continued reduction in short-term liquidity, the onshore Yuan’s borrowing costs saw declines: the SHIBOR O/N, 1W and 2W dropped -0.42, -0.60 and -0.10 BP on Thursday from a day ago. Normally, when the PBOC removes cash from the market, Yuan’s funding costs would increase.

Over the past two weeks, we have seen such inconsistent moves between short-term liquidity injections and short-term Yuan borrowing costs. The PBOC added a net of 95.5 billion Yuan through reverse repos in the week of Oct 17th to 23rd and 595 billion Yuan in the week of 24th to 30th. However, the short-term SHIBOR remained on an upward trend, which was unusual.

Data downloaded from Bloomberg; chart prepared by Renee Mu.

This is likely caused by Yuan exchange rates. The Chinese currency has lost -0.65% against the U.S. Dollar offshore and -0.70% onshore from October 17th to 30th, mostly driven by imminent Fed rate hike expectations. Amid the Dollar advance, Chinese investors and companies show less incentive to sell foreign currencies to commercial banks and eventually reduce the Central Bank’s foreign exchange holdings. As a result, the Central Bank pays less Yuan to commercial banks in exchange of foreign currencies, and this reduces the monetary base for the Yuan.