Ares Capital (ARCC) is an attractive big-dividend (9.9%) Business Development Company (BDC) trading at a discounted price. As shown in our recent report, Big Dividend BDCs: Ranking the Best and Worst, Ares price dropped (-3.2%) during the recent market-wide selloff of big dividend securities, and it now trades at an 11% discount to its Net Asset Value (NAV). It just announced earnings a few days ago, and despite the risks, such as heightened short-interest, an increasingly hawkish fed, and management conflicts of interest, we believe Ares is an attractive long-term investment for income-focused investors because of its big dividend, recently discounted price, and attractive fundamentals.

About

Ares’ objective is to generate current income and capital appreciation through its debt and equity investments. It’s a regulated investment company and BDC, which means it’s required to distribute at least 90% of its taxable income to shareholders (note: distributing at least 90% allows Ares to avoid corporate income tax on distributed taxable income). As a side note, BDCs were created by Congress in 1980 to provide public investors another means to invest in private US business, typically small and middle market companies.

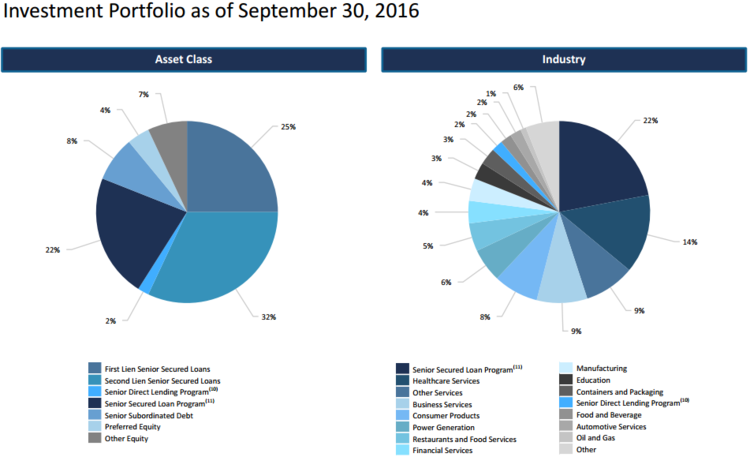

As shown in the following chart, Ares investments are diversified across multiple asset classes and industries.

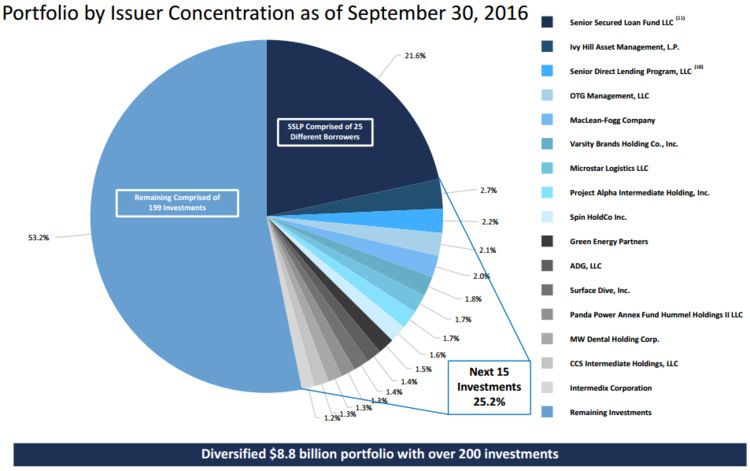

And for added perspective, this next chart shows Ares $8.8 billion investment portfolio is diversified across multiple issuers.

Also worth noting, Ares is externally managed by Ares Capital Management LLC, a subsidiary of Ares Management, L.P. (ARES), a publicly traded, alternative asset manager. We’ll have more to say about external management team later.

Valuation and Fundamentals

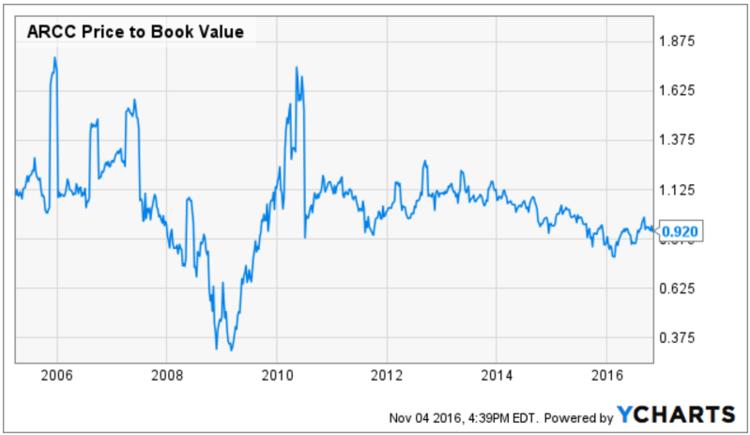

From a valuation standpoint, Ares is not unattractive. For example, the following chart shows that Ares is currently trading at a discount to its book value.

And while such a discount can be viewed as a risk (i.e. it can be more challenging for a BDC to raise capital when its Price to Book is low), we view it as a positive indication of stock price appreciation potential. For example, part of the reason the price has declined is due to near-term expectations surrounding its upcoming acquisition of American Capital (more on this later).