Over the past decade, alternative assets (private equity, real estate, hedge funds, and complex debt instruments) have become increasingly popular, with assets under management nearly quadrupling.

The future is bright as well. PricewaterhouseCoopers expects total alternative assets to reach close to $14 trillion by 2020, growing by about 9% annually.

Given the complex nature of these investments, and the fact that most are only accessible to high income and high net worth individuals, many dividend investors might be drawn to publicly-traded alternative asset managers such as The Blackstone Group (BX), The Carlyle Group (CG), and Icahn Enterprises (IEP).

However, while the financial media may make these legendary asset managers seem like masters of the universe, that doesn’t necessarily mean that income investors can do well owning these complex financial stocks. In fact, many of these complicated businesses violate Warren Buffett’s top piece of investment advice to remain within one’s circle of competence.

Let’s take a look at The Blackstone Group, the largest of the private equity/alternative asset managers, to see if most dividend investors are better off staying away from this industry or if Blackstone Group’s 5.7% dividend yield could be worth pursuing for our Conservative Retirees dividend portfolio.

Business Description

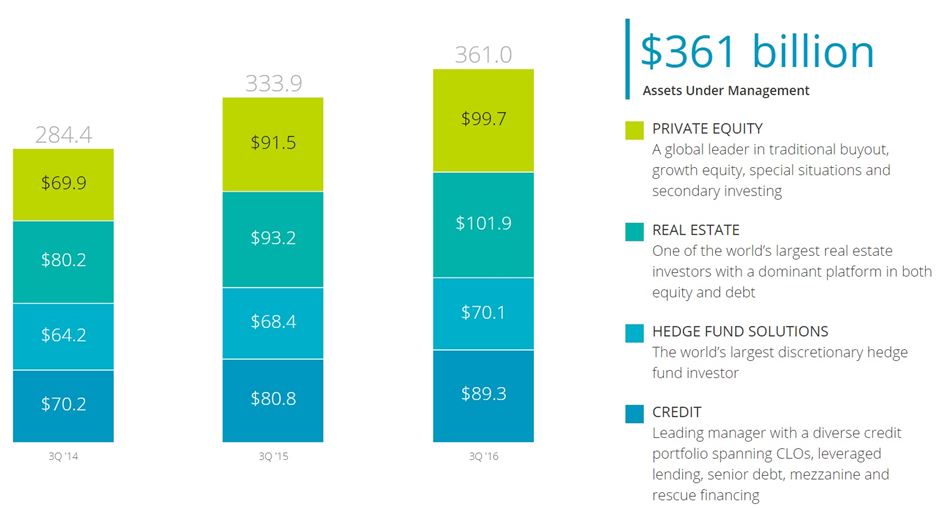

The Blackstone Group (BX) is the world’s largest alternative asset manager with over 2,200 employees in over 20 countries, managing $361 billion of investor capital.

The firm specializes in private equity (owning private companies), real estate, hedge funds, and investing in private debt. Blackstone earns its money by charging investors a base management fee (about 0.8%) plus performance fees (% of profits above a certain hurdle rate), which in this industry can be extremely lucrative.

(Click on image to enlarge)

Source: Blackstone Group

In 2015, the vast majority of the firm’s revenue and operating profits came from its real estate and private equity divisions, which has historically been where Blackstone’s expertise lies.

| Business Segment | 2015 Revenue | 2015 Operating Income | % Of Revenue | % Of Operating Income |

| Real Estate | $1.791 billion | $948 million | 42.2% | 44.9% |

| Private Equity | $1.382 billion | $656 million | 32.5% | 31.0% |

| Hedge Funds | $590 million | $296 million | 13.9% | 14.0% |

| Credit | $485 million | $213 million | 11.4% | 10.1% |

| Total | $4.248 billion | $2.113 billion | 100% | 100% |

Source: Blackstone Group Supplemental Presentation

Business Analysis

Blackstone is the biggest, most diversified name in alternative asset management, having been founded in 1985 by Stephen Schwarzman, who continues to serve as Chairman and CEO.

The company prides itself on taking a long-term approach to investing partner capital, including long lock-up periods on its funds that prevent Blackstone from having to sell at the bottom of market panics.

This has allowed the company’s funds over a five, 10, and 15 year period to generate returns of about 15% net of fees, which is among the best of any asset manager.

The long-term success of Blackstone has resulted in truly astounding growth, with over $200 billion in new capital being raised in just the last five years alone. To put that in context, this amount of new capital inflow is more than its next four largest rivals combined.

The massive size of Blackstone not just means a lot of fee income, but also serves as a major competitive advantage. Specifically, the company is a wide moat business thanks to its excellent reputation and access to some of the world’s best fund managers.