If more people desire a certain thing, in a free market the price of that certain thing will go up regardless of any possible inherent value. Indeed, that is how market consensus is supposed to work, the backbone of efficient markets. I don’t believe that markets are or ever can be perfectly efficient, especially in the current age where assumptions are passed around as gospel with nary a challenge whispered or otherwise. What were, for example, oil investors thinking in early July 2008? Whatever it was, it was clearly wrong.

John Maynard Keynes wrote about liquidity preferences in his General Theory, assigned to consumers as an answer for why they might “hoard†money or currency. There were, Keynes presumed, three structural parameters that governed their choices, each with a specific rationale or tradeoff to be assumed. Among them was opportunity, meaning that consumers will hold cash for a better future opportunity unless the perceived return on current opportunity can overcome that preference.

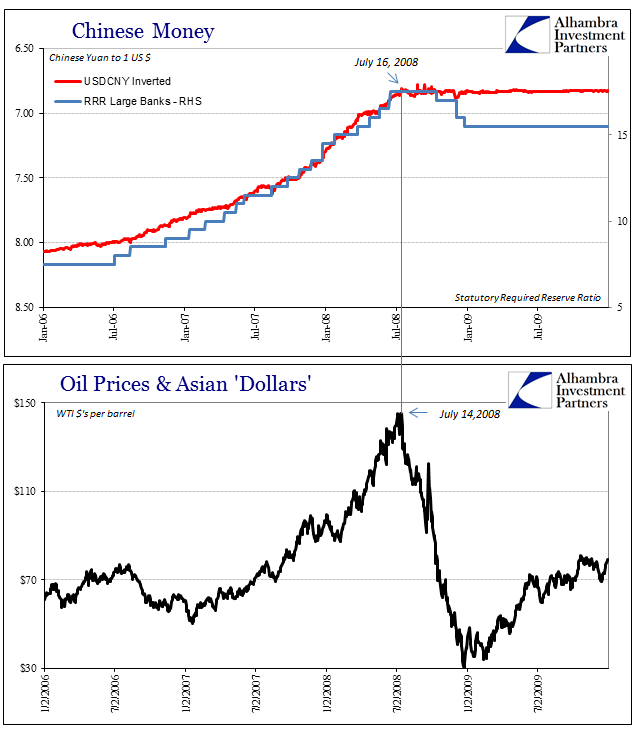

What oil investors in the first half of 2008 missed was, I believe, liquidity preferences, but not those of consumers. They were not alone, of course, as almost everyone did, too, including people like Ben Bernanke who by all rights should have known better (that was his whole job). The eurodollar futures market, for one, had been warning monetary officials for more than a year and a half by the time oil prices crashed (the first time).

Absent opportunity the paradigm shifts, and past a certain critical threshold shifts dramatically and dangerously. There is a balance to where opportunity and risk rebalance entirely from one to the other. It is long before that point where central banks not only are supposed to intervene but had claimed for decades that they would without question.

In the middle of 2008, the desire for liquidity turned truly desperate to the point of panic largely upon the point that oil investors did not foresee – the Fed did not know what it was doing. Markets being forgiving, however, the Fed was given another chance only to similarly squander it. Thus, for liquidity preferences, 2008 was panicked doubt whereas 2011 was resignation. The difference in liquidity preferences between them was merely time.