This week brings a loaded economic docket to global markets, with an emphasis on what’s become a favorite pain point of inflation. The week has already started on a brisk note as a 47-year high was recorded in the German IFO ‘Business Climate’ survey, and the net reaction was a quick gust of strength in the Euro and a burst-lower in Gold prices.

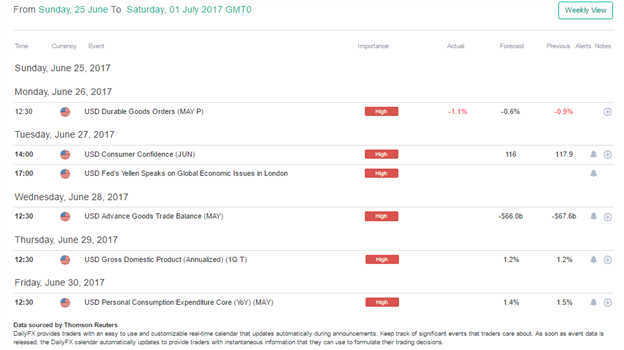

But also on the calendar for this week is pertinent data for every day through Friday, along with some key Central Banker speeches that will likely elicit considerable attention. Fed Chair Janet Yellen is set to speak in London tomorrow afternoon, and we also hear from Williams, Harker and Kashkari throughout the day on Tuesday. John Williams speaks again on Wednesday and we hear from James Bullard on Thursday. We also have the ECB forum kicking off today, which will see BoE Governor Mark Carney, ECB President Mario Draghi and BoJ Governor Haruhiko Kuroda offer comments on Wednesday. Below, we’re looking at the DailyFX Economic Calendar with the high impact events for the U.S. Dollar for the week ahead.

DailyFX Economic Calendar: High Impact Events for the U.S. Dollar for the week of June 26th, 2017

U.S. Dollar Longer-Term Bearish Trend Channel Remains Intact

Since the Federal Reserve’s rate hike earlier in June, the U.S. Dollar has been trying to move into a bullish trend, albeit tenuously. On the morning of that rate hike, a series of bad U.S. data prints had brought-on a fresh seven-month low in DXY: But after the hike, buyers have been trying to push the Greenback higher as we can see as indicated by the ‘higher-high’s on the hourly chart below.

Chart prepared by James Stanley

Current resistance is showing in DXY around the 50% Fibonacci retracement of the May, 2016 to January, 2017 major move at 97.87, and this level is confluent with the mid-line of the bearish channel that’s defined DXY price action for much of the year, so far. Since this level of resistance has come back into-play, bulls have been losing ground, giving the appearance of oncoming bearish continuation of the ‘bigger picture’ trend. On Thursday of last week, we had looked at support structure in USD with emphasis on the 97.50 level for a potential ‘higher-low’. That support has not been able to hold, and at this stage, it appears that near-term bearish momentum is beginning to mesh with the longer-term bearish trend.