You can add SocGen’s asset allocation team to the list of folks who think it’s time to reduce risk ahead of central banks’ attempt to normalize policy.

Although they’re only downgrading risk assets to “Neutral†(as opposed to our “get out while you still can†reco), SocGen thinks that in continuing to rise, markets are defying a “quite clear†message from policymakers: namely that they are now concerned about how history will remember their efforts.

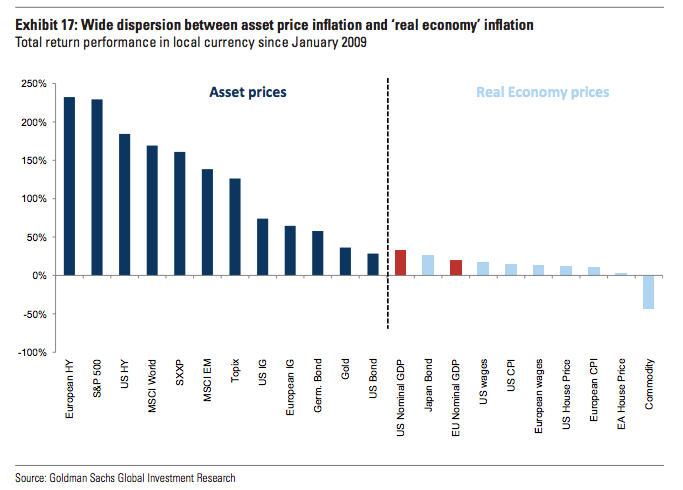

Although policymakers undoubtedly realized what was likely to happen in risk assets when they began pumping trillions in liquidity into the system, it’s conceivable (indeed, it’s likely) that they underestimated the multiplier effect embedded in the transmission channel from ultra accommodative policies to financial assets. At the same time, they seem to have overestimated the multiplier embedded in the transmission channel from those same policies to the real economy. In combination, those miscalculations led directly to this state of affairs eight years on:

And so, facing what SocGen correctly calls “skyrocketing asset valuations,â€Â the experiment in accommodation will be unwound, with consequences that are simply unknowable ahead of time. Of course if we had to guess, the deleterious effect this will have on risk assets will ultimately force central banks to step right back in to rescue the bubble before it bursts completely, thus proving that “QE-finity†is real – but that’s another story.

Read more from SocGen below on why “when markets look at the blue sky with sunglasses,†it’s time to reduce risk…

Via SocGen

Since 2009, we in the SG asset allocation team have communicated regularly on our positive stance on risk assets. Our rationale has been that central banks’ fiscal and especially monetary reactions have regularly superseded expectations and have been powerful enough to counteract the worst deflationary forces successfully. After all, G4 central banks, whose total balance sheet currently stands at USD19,462bn, have injected a combined USD12,540bn since the Lehman Brothers collapse! The impossible fight has been won and even the euro area is showing signs of progress across the board, can you believe it?

We believe it is the right time, when markets look at the blue sky with sunglasses and when the trend and carry is your friend, to recommend downgrading risk assets (corporate bonds, equities); to Neutral for equities and UW for corporate bonds, in favour of short and long dated bonds, and gold, with a high remaining content of EM and euro (the latter being still cheap in spite of its recent rise).

Considering the key triggers that are expected in the last quarter of 2017 (synchronised Fed and ECB tightening), we see cause for concern in the current combination of complacency (low cross-asset volatility and low single-asset-class volatility, high net shorts on volatility, accelerated flows into illiquid assets like Credit), much lower affordability indices on residential real estate, and high financial asset valuations.

Â

Central banks are shifting away from their inflation concerns to other preoccupations: skyrocketing asset valuations, an improved growth outlook and reduced policy uncertainty. The markets are pushing back on what is actually quite a clear message from central banks that don’t want to see a repeat of the errors made in the past by the Bernanke’s and Greenspan’s of this (monetary) world: staying behind the curve unnecessarily for too long – we won’t be.