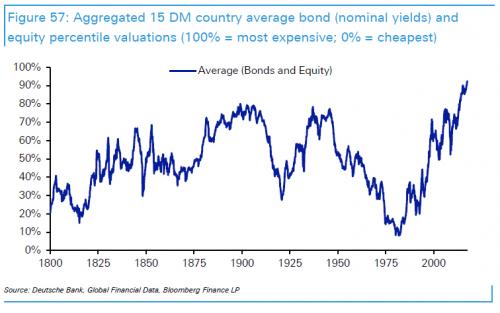

In an extensive, must-read report published on Monday by Deutsche Bank’s Jim Reid, the credit strategist unveiled an extensive analysis of the “Next Financial Crisis”, and specifically what may cause it, when it may happen, and how the world could respond assuming it still has means to counteract the next economic and financial crash. In our first take on the report yesterday, we showed one key aspect of the “crash” calculus: between bonds and stocks, global asset prices are the most elevated they have ever been.

With that baseline in mind, what happens next should be obvious: unless one assumes that the laws of economics and finance are irreparably broken, a deep recession and a market crash are inevitable, especially after the third biggest and second longest central bank-sponsored bull market in history.

But what will cause it, and when will it happen?

Needless to say, these are the questions that everyone in capital markets today wants answered. And while nobody can claim to know the right answer, here are some excerpts from what DB’s Jim Reid, one of the best strategists on Wall Street, thinks will take place.

Below we present the key excerpts from his must read report;

* * *

We think that the post Bretton Woods (1971-) global financial system remains vulnerable to financial crises. A simple internet search of financial crises through history (Figure 1, LHS chart) confirms that the frequency has increased over this period. Examples include the UK secondary banking crisis (1975), the two Oil shocks (1970s), numerous EM defaults (mid-1980s), US Savings and Loans mass failures (late 80s/early 90s), various Nordic financial crises (late 80s), Japanese stock bubble bursting (1990-), various ERM shocks/devaluations (1992), the Mexican Tequila crisis (1994), the Asian crisis (1997), the Russian & LTCM crisis (1998), the Dot.com crash (2000), the various accounting scandals (02/03), the GFC (08/09) and the Euro Sovereign crisis (10-12).

A more quantitative search backs this up (Figure 1, RH chart). We show the number of DM countries (%) in our sample back to 1800 experiencing one of the following on a YoY basis; -15% Equities, -10% FX, -10% Bond move, a sovereign default, or +10% inflation. This is our crisis/shock indicator. 0% equals no country with one of these conditions met, 100% equals all in our sample with one being met.