With no North Korean nuclear test over the weekend contrary to a Friday morning rumor, S&P futures rebounded and edged higher as European stocks gain, led by Spanish shares after mass demonstrations in favor of Spanish unity and speculation Catalonia may back down on unilateral independence demands, while Chinese mainland stocks reopened catching up to gains missed during the holiday week following last weekend’s RRR cut.

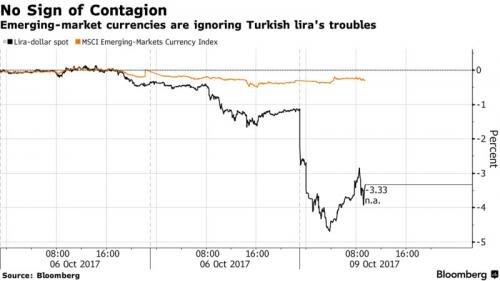

World shares rose to start the week, with Chinese stocks hitting 21-month highs and the German index setting a new record, while political uncertainty triggered big moves in sterling, the Turkish lira and Spanish debt. US futures are also pushing higher in anticipation of the start of Q3 earnings season which begins later this week, with a number of Wall Street banks including JPMorgan, BofA and Citi set to report. While equities are open, the US bond market is closed today for the Columbus day holiday, while Asian markets were relatively quiet following holidays in Japan, South Korea and Taiwan.

European stocks climbed at the start of a week in which investors were closely watching developments in Catalonia as well as U.S. earnings season kicks off. The Stoxx Europe 600 Index adds 0.23%, following four straight weeks of gains. All industry groups except miners climb. The IBEX 35 Index is up 1% as a senior member in the Catalan administration calls for dialogue with Spain, although the gauge is still down 1.2% since Catalans voted for independence in an illegal referendum. After a weekend of mass demonstrations in favor of Spanish unity, Raul Romeva, foreign affairs chief for the separatist government in Barcelona, insisted that the door was open for talks if Prime Minister Mariano Rajoy was willing to grasp the opportunity

As Bloomberg breaks down local markets, 18 out of 19 Stoxx 600 sectors rise; 407 Stoxx 600 members gain, 171 decline. Top Stoxx 600 outperformers include: CaixaBank +2.6%, Centamin +2.5%, TDC +2.4%, Man Group +2.4%, Metro Bank +2.0%. The Stoxx Euro 600 Index also received a boost from data showing German industrial output rebounded from a summer lull with its best month in six years. The euro nudged higher, while most European bonds rose. Gold climbed and crude oil erased earlier gains.

“As regards Catalonia, it is difficult to have much conviction with respect to the eventual outcome,†JPMorgan Chase & Co strategist Mislav Matejka said in a note. “However, we believe that this will be seen as a localized issue, where the dips should be bought.â€

Sterling rose 0.6 percent to $1.3112 on reports that British Prime Minister Theresa May, facing threats to oust her, might sack her foreign minister, Boris Johnson. Reports stated that the UK is said to be searching and hoping for the best, but is also continuing making preparations in case it should end up with no deal in Brexit talks. (Telegraph) Further to this, PM May is set to warn EU leaders today that Britain will make no more concessions on Brexit until they compromise on opening trade and transition talks. (Times) UK PM May reportedly suggested over the weekend that she is prepared to demote Foreign Secretary Boris Johnson as part of a cabinet rejig.However, separate reports suggest that if May was to fire him, he will simply say ‘no’, according to his allies.

“If Boris Johnson were to leave or be demoted as the weekend press is suggesting, that would be showing May’s leadership and that her vision of Brexit is the one that (the government) will be going forward with and that markets should be aligned to,†said Viraj Patel, an FX strategist at ING Bank in London.

The most notable event in European trading was the plunge in Turkey’s lira which slumped to a record low against a basket of currencies including the euro and the dollar, and the nation’s stocks slumped, after U.S. and Turkey each suspended visa services for citizens looking to visit the other country.

Also in Europe, German Chancellor Merkel’s CDU/CSU agreed on refugee cap issue which clears a major hurdle in pursuing coalition discussions.Germany and France reportedly dashed UK hopes of fast-track talks on transition deal and said that a divorce bill must be resolved first.EU was reported on Friday to significantly step up backroom Brexit talks with Labour Party over concerns PM May’s government will fall.Pressure on the BoE to raise interest rates may be building more rapidly than first thought after a mistake by the ONS led to domestic inflation being understated with companies’ employment costs rising faster than previously expected.

In Asia, the MSCI Asia Pacific Index added 0.1% to 163.41 as of 11:40 a.m. in Hong Kong, with Australian banks leading gains after a politician said he’s opposed to a regional levy.Stocks in New Zealand set a new record while the local dollar slipped as the major political parties vied to form the new government. The S&P/NZX 50 benchmark rose 0.4 percent, topping 8,000 for the first time. In Hong Kong, the Hang Seng Index slipped after hitting a 10-year high on Friday.

Chinese stocks rose as trading resumed after a week-long holiday but an Asia-wide benchmark was little changed as markets in Japan, South Korea and Taiwan were closed. On their first day of trade after a week-long holiday, Chinese blue-chip stocks touched their highest levels since late 2015, partly in a delayed reaction to a targeted cut in the amount of cash some banks must hold in reserve bank announced a week ago. Mainland Chinese markets rose Monday, although the advance faded as banks were unable to hold on to much of their early gains. The Shanghai Composite Index closed up 0.8% at 3,374.38 after rising as much as 1.8% to touch the highest since January 2016, while the Shenzhen Composite Index added 1.3%, the most since Aug. 28. Financials also took the lead in mainland China, where stocks tracked last week’s advance in offshore trading, after the central bank’s decision to cut reserve ratios.

#Shanghai Composite closed 0.76% higher at 3374, after surging above 3400 intraday to 21-month high pic.twitter.com/Cnwon0mtR1

— YUAN TALKS (@YuanTalks) October 9, 2017

Also notable was the big move higher in Chinese rates, with 10Y futures closing down 0.36%, the biggest one day move in 2 months. A big reason for this was the surge in the Yuan, which jumped over300 pips, pushing the USDCNH below 6.62 from nearly 6.66 earlier.

Also worth noting that on Monday, Business activity in China’s services sector grew at its slowest pace in 21 months in September as the pace of new business cooled, according to the Caixin Markit PMI survey, in contrast with official data from the National Bureau of Statistics (NBS) showing a faster pace of growth. Specifically, the Chinese Caixin Services PMI printed at 50.6 in September vs. Exp. 53.1 (Prev. 52.7); a 21-month low.

Oil trades around $50, as OPEC Sec-Gen Mohammad Barkindo says that oil producers are succeeding in re-balancing oversupplied market, though they may need to take further steps to sustain recovery into 2018. Production is increasing at Sharara, Libya’s biggest oil field, after it re-opened on Oct. 4, and is now expected to produce up to 250,000bbls/day/