S&P futures are again modestly in the green as European shares hold steady ahead of a meeting of the Catalan regional parliament and a possible declaration of independence by Catalan leader Puigdemont, while Asian shares rise a the second day. The dollar declined for the 3rd day, its losses accelerating across the board amid growing concerns that Trump’s tax reform is once again dead following the Corker spat and a rejection from Paul Ryan, with the move gaining traction after China set the yuan’s fixing stronger for the first time in seven days. Monday’s sell-off in Turkish assets seemed to have little follow-through, with emerging-market currencies all trading higher and Treasuries steady. Traders are also waiting for minutes from the Federal Reserve’s last meeting, which may provide more details on the path of interest rates and balance sheet tapering.

“The weak dollar is a cue for investors that the U.S. Fed will not be aggressive in raising interest rates and this supports the outlook for a strong equities market,” said Cristina Ulang, head of research at First Metro Investment Corp. in Manila. “We will see a U.S. rate increase in December but it’s not going to be sharp since we aren’t seeing runaway U.S. economic growth.”

Asia stocks advanced as traders in Japan and South Korea returned from holidays, pushing the regional benchmark to a three-week high amid a broad weakness in the dollar. The MSCI Asia Pacific Index gained 0.7% to 164.49, its highest close since Sept. 20. The biggest boost came from Samsung Electronics which also helped South Korea’s Kospi advance 1.6%. In Japan, the Topix rose to its highest close in more than a decade, driven by a string of positive economic data both at home and abroad. The Asia-wide gauge has rallied 22 percent so far this year, on course for its best performance since 2009. It’s still trading at the biggest discount to the S&P 500 Index in 15 years in terms of price-to-book.

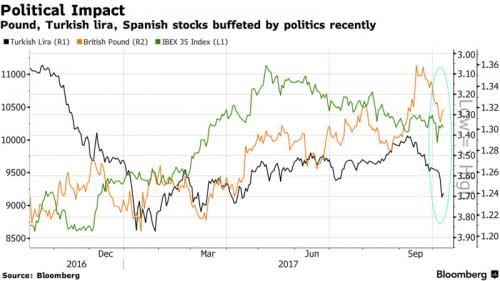

All eyes are on Europe however, and Spain in particular, where Catalan lawmakers will meet today to consider a declaration of independence that risks an ironclad backlash from Madrid. Attention will focus on the form of words used by Catalan President Carles Puigdemont, who is due to address the parliament in Barcelona at 6 p.m. The IBEX fell alongside most national gauges across Europe. The common currency gained for a third day. It is Spain’s biggest political crisis since an attempted military coup in 1981. Madrid’s IBEX stocks index drooped 0.5 percent early on and it is now down almost 9 percent since May, though a sharp rise in the euro has also taken a toll.

“We have not witnessed any relevant statement or signal by the separatists that would hint at a change of strategy ahead of today’s discussion in the Catalonian parliament,†economists at Barclays wrote.Â

“Consequently, at this point, it seems likely that Catalan President Carles Puigdemont remains on track to announce a unilateral declaration of independence as early as today.â€

“Rather than a full universal declaration of independence, we may see a ‘symbolic statement’ from the Catalan government,†said Fabio Balboni, economist at HSBC Bank Plc. “Signs of disagreement are starting to emerge within the regional government, with more moderate members fearing the consequences of a further step towards independence, given the lack of support from the EU, and moves by some banks and firms to leave Catalonia.â€

Despite the Spain jitters, The euro remained resilient, rising to a one-week high as data showed German exports had surged in August. Traders were also still upbeat on the currency after one of the European Central Bank’s German policymakers called for an end to its stimulus.

Elsewhere, Turkey’s lira recouped some of yesterdays losses even as the U.S. signaled the crisis between the two countries could drag on. Gold rose as the greenback weakened, and West Texas oil held gains near $50 a barrel before U.S. government data forecast to show crude inventories extended declines for a third week. Japan’s Topix index closed at the highest since July 2007 and Korean stocks staged a catch-up rally after a week-long holiday.

Turkey also got some help from a weaker dollar which was down for a third straight day. The dollar index, which tracks the greenback against six major rivals, dropped 0.2 percent to 93.533 and away from Friday’s almost 3-month peak. It gave the Turkish lira a breather having been sent sprawling to a nine-month low on Monday after the United States and Turkey scaled back visa services.

Meanwhile, Mexico’s peso hovered at its weakest in more than four months, ahead of the latest round of talks over the North American Free Trade Agreement (NAFTA) on Wednesday.

Over in Asia, the offshore Chinese yuan rate surged to its strongest levels in more than two-weeks. The central bank had also set a firmer-than-expected official rate, suggesting authorities are keen to keep the currency in check ahead of next week’s key national leadership meeting.

In commodities, Crude oil prices edged slightly higher, supported by OPEC comments signaling the possibility of continued action to restore market balance in the long-term. But gains were seen as limited as oil production platforms in the Gulf of Mexico started returning to service after the latest U.S. hurricane forced the shutdown of more than 90 percent of crude output in the area. Brent crude inched up 1 cent to $55.80 a barrel. U.S. crude added 2 cents to $49.60. Gold prices hit their highest in more than a week, though gains were capped as expectations of another U.S. interest rate hike this year limited appetite. Spot gold added 0.2 percent to $1,286.52 an ounce

Rate markets were largely unchanged, with the yield on 10-year Treasuries declined one basis point to 2.35 percent. Germany’s 10-year yield dipped one basis point to 0.44 percent, the lowest in two weeks. Britain’s 10-year yield was unchanged at 1.357 percent, the lowest in a week.