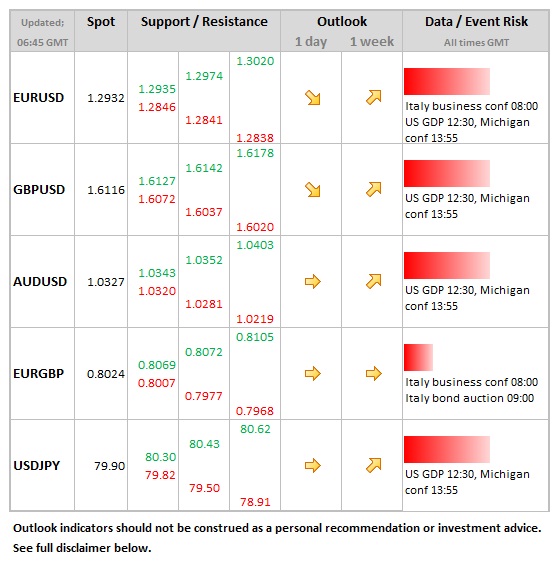

Data/Event Risks

Data/Event Risks

- USD: The first read of Q3 GDP and Michigan confidence data. The market looks for annualised growth of 1.8%. Stronger data would help the dollar, but only modestly so. Focus remains on labour market so strong data not likely to change Fed’s stance on policy.

- EUR: Focus on Italy, but not likely rock the euro. Business confidence together with sales of index-linked and zero coupon bonds.

Idea of the Day

Even though market is looking for 1.8% (median) annualised growth in the US for the third quarter, there is an upward skew to the forecasts, with nearly a quarter of institutions going for 2.0%. This could give the dollar a lift into the end of the week, especially with stocks on the defensive during Asian hours, but with 2 week to go until the election, the dollar could struggle to rally on a sustained basis.

Latest FX News

- USD: Stocks moving into positive territory into the close, but only just. Notable how risk-on, risk-off breaking down, with yen weaker, Aussie holding up despite stocks at lows for the month.

- EUR: Latest data showed German consumer confidence rising further,

- NZD: Kiwi weaker on latest trade data, showing headline deficit at widest for nearly 2 years (NZD 888mln). AUD/NZD firmer, but still within range of the week at 1.26.

- AUD: No major news overnight, but Aussie struggling into the end of the week as risk aversion prevails. AUD/USD holding near to the 1.03 level. Avg. past 3 months has been 1.04.

- JPY: Sep National inflation data recorded -0.3% YoY (from -0.4%), with Tokyo measure for Oct at -0.8%. Yen firmer o/n, on generalised risk aversion and lower stocks, USD/JPY testing 80.00 level.