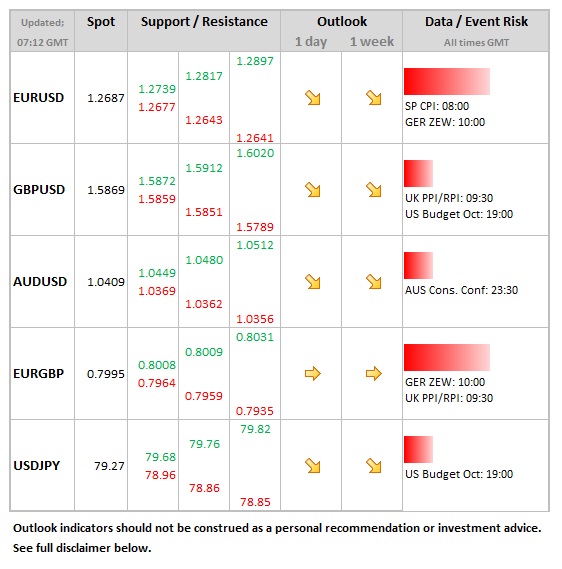

Data/Event Risks

Data/Event Risks

- USD: Fiscal cliff discussions rank ahead of economic news in the near term. The president will meet House and Senate leaders on Friday. Both sides are sounding hopeful of a deal, but it remains to be seen if compromise can be achieved.

- EUR: Second-tier releases today, with Spanish and Italian CPI followed by German ZEW (see how to trade it with EUR/USD). Ecofin meeting tonight in Brussels, with Greek aid at the top of the agenda.

- GBP: Lots of event-risk in coming days, with RPI/PPI today, followed by jobs and wages data tomorrow and retail sales on Thursday. Should labour market and spending reports indicate that the economy is faltering then sterling will react negatively.

Idea of the Day

Clear disagreements exist within Europe regarding Greece, which weighed on both the euro and risk assets overnight. Not helping was news that Microsoft President Sinofsky was departing after 23 years. No need to fight the tape at present – both the dollar and the yen are creeping higher, while the euro consistently slides.

Latest FX News

- EUR: The gradual downtrend continued overnight amidst fresh concerns on Greece. Lagarde claimed more work needed to be done on Greek debt sustainability over coming days. Key technical levels down near 1.2640.

- JPY: Benefitted from more risk-averse backdrop, despite confirmation of plunge in industrial production in September. Lots of discussion in Tokyo regarding additional monetary action, including the purchase of foreign bonds by the BoJ.

- AUD: Suffered for a time alongside weak Asian equity markets. Weak NAB business survey contributed to the sombre mood. All things considered, still looks well-supported.

- CNY: Reached a 19yr high yesterday, helped by decision to raise quota for RQFII by RMB 200bn. Note that spot RMB trades at the maximum 1% premium to the reference rate. Indeed, reference rate has barely changed in recent weeks. Expect PBOC to resist pressure for yuan appreciation.