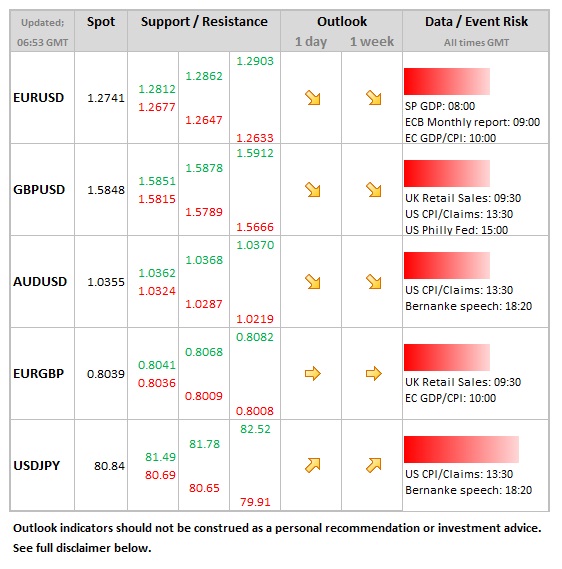

Data/Event Risks

Data/Event Risks

- USD: Watch fiscal cliff debate closely as hotting up already. Obama will ask Republicans for USD 1.6trln in tax cuts, double what he demanded in the summer of 2011. Plenty of data as well today, including claims, CPI and Philly Fed.

- EUR: A busy agenda, with SP and IT GDP, before EU GDP at 10:00. EU still at loggerheads with IMF re Greece – this remains critical for the euro. Europe effectively on strike yesterday, amidst widespread social unrest at perpetual austerity.

- GBP: Retail sales the main focus today. Recent months suggested UK consumer doing better. If reconfirmed today, then the pound may recover some of yesterday’s losses.

Idea of the Day

Lots of forex themes in play yesterday – yen weakness despite big down-day in stocks, euro-short squeeze, and sterling softness after Inflation Report. Volatility in the majors likely to continue short term. Stay alert to rapid mini-trend changes. Favour the dollar while risk appetite wanes. Gold looks vulnerable.

Latest FX News

- EUR: Classic short-squeeze in the morning, despite dreadful data out of Spain and Italy. Even so, traders should be troubled by the uncertainty re Greece aid. IMF clearly unhappy with EU approach. Euro has done well vs. Aussie, sterling and yen over the past 24 hours – can it continue?

- JPY: A huge victory for yen shorts yesterday and overnight, following news that Noda has called an election for mid-December. Japan desperately needs a weaker currency, because corporate sector specifically, and economy more generally, is in dire trouble. LDP will push BoJ very hard if elected.

- GBP: Suffered after the Inflation Report. King expresses concern re pound resilience and leaves door open for more QE. Still, the damage to the currency was quite minor.

- AUD: Much-trumpeted resilience has given way slightly, with Aussie down to 1.0350 overnight. Lots of sell stops triggered; big dump in equities not helpful either. More weakness likely near term if risk repulsion continues. But be careful because SWFs probably lurk at lower levels.