After five consecutive daily losses on the MSCI world stock index and seven straight falls in Europe, there was finally a bounce, as investors returned to global equity markets in an optimistic mood on Thursday, sending US futures higher after several days of losses as global stocks rebounded following a Chinese commodity-driven rout.Â

The House is poised to vote, and pass, on tax legislation although what happens in the Senate remains unclear. European shares rebounded for the first time in eight sessions, following Asian stocks higher as the global risk-off mood eased. The euro, Swiss franc and yen all weakened as the dollar edged higher. “After five or six days of steady selling you have got people coming back in looking for bargains,†said CMC Markets’ Michael Hewson. “I think it’s temporary though. We haven’t had a significant sell off this year and the fact of the matter is that equity markets have done so much better than anyone dared to envisage.â€

As Bloomberg echoes, “investors seem to be regaining their appetite for risk after several days of global declines in stocks and high-yield credit that had many questioning whether the selloff could become a rout.”

Still, investor concern over the progress of a massive U.S. tax reform plan showed no sign of abating as two Republican lawmakers on Wednesday criticized the Senate’s latest proposal. U.S. President Donald Trump hit back, tweeting that “Tax cuts are getting close!â€

“If we look at what the markets are focusing on, it’s still very much the tax cut debates in the U.S., and how much progress there’s going to be on this front,†Barclays’ Mitul Kotecha told Reuters.

Indices in Tokyo, Shanghai and Hong Kong and Seoul all rallied overnight, while London, Frankfurt and Paris started 0.3-0.4% higher as cyclical stocks which had driven the sell-off made a comeback. In Japan the Topix index ended its longest losing streak in a year, rising 1% with technology stocks providing the biggest boost, and the Nikkei 225 advances 1.5%. The ASX (+0.2%) also managed to shake off its early losses, closing higher with the energy sector outperforming as consumer staples and utilities weighed. Chinese stocks edged lower despite a massive cash injection by the PBOC, while the Hang Seng moved higher. Hong Kong stocks rebounded from their worst day in four weeks, as insurers led by Ping An Insurance Group Co. jumped on optimism that rising bond yields will boost investment income. Tencent Holdings climbed after posting its fastest revenue growth in seven years.

China’s sovereign bonds finally rebounded, advancing after the central bank boosted cash injections by the most in 10 months, fueling speculation that the authorities are looking to stabilize sentiment after a debt selloff. Having flirted with 4% in recent days, the yield on 10-year government notes dropped 3 basis points to 3.95%; the 5-year yield fell 1 basis point to 3.95%. The 10-year yield surpassed 4% this week for the first time since 2014. The People’s Bank of China added a net 310 billion yuan ($47 billion) through reverse-repurchase agreements on Thursday, bringing this week’s open-market operation additions to 820 billion yuan, also the most since January.

European stocks bounce back from a seven-day rout – the longest losing streak of the year – that had erased almost 400 billion euros ($471 billion) from the value of the region’s benchmark. The Stoxx Europe 600 Index adds 0.7%, following gains in Asia and climbing from a two-month low. All national benchmarks in the region are in the green, except those in Italy and Greece. Most industry groups also rise, with automakers rebounding from an eight-day slump on data showing European car sales grew in October. Financial services firms and builders were among the biggest gainers in the broad advance of the Stoxx Europe 600 Index.

There was some relief too that oil prices had pulled out of what had been a near 5 percent drop and that upbeat U.S. data on Wednesday had helped the dollar halt the euro’s sharp recent rise.

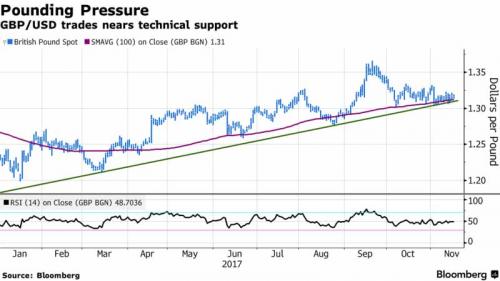

In currencies, the pound fluctuated as Brexit rhetoric rumbled on, and data showed U.K. retail sales barely rose in October. Concerns about Brexit continue to mount: an article in ‘The Sun’ newspaper, stated that UK PM May, could increase her divorce bill offer to the EU in December; deal would add GBP 20bln to the GBP 18bln said to already be on offer. Source reports indicate that EU is said to reject UK bid for `bespoke’ trade deal, according to Politico. BoE’s Carney states that the Bank will do whatever they can to support the UK economy during the Brexit transition period. Chancellor Hammond said to stick to fiscal rules and resist demands for spending surge in upcoming UK budget. Michael Gove is reportedly facing a Conservative party backlash as he is accused of using the cabinet to audition for UK Chancellor.

The dollar index was slightly higher on the day at 93.828 having hit four- and five-week lows against the yen and euro. The euro was down around 14 ticks at $1.1760 retreating from a one-month top of $1.1860 on Wednesday. Havens underperformed on Thursday, with gold trading little changed, and the yen and Swiss franc among the worst-performing major currencies. The Swiss franc decreased 0.3 percent to $0.9918, the largest dip in more than two weeks.

Commodities largely stabilized as China’s central bank boosted the supply of cash in the system by the most since January, though oil eventually reversed a gain. Gold edged 0.1% lower to $1,277.29 an ounce. It reached $1,289.09 overnight, its highest since Oct. 20. Oil prices gained despite pressure after the U.S. government reported an unexpected increase in crude and gasoline stockpiles. They had lost ground to this week’s International Energy Agency (IEA) outlook for slower growth in global crude demand.

European government bonds took their cue from the U.S. benchmark, turning lower as the yield on 10-year Treasuries increased. Bond markets saw a broad rise in yields after mostly upbeat U.S. economic news on Wednesday had added to expectations the Federal Reserve will hike interest rates again next month as well as multiple times next year. Two-year Treasury yields US2YT=RR crept to fresh nine-year peaks in European trading, though significantly the U.S. yield curve remained at its flattest in a decade. European yields nudged higher too but the standout there was a fall in the premium investors demand to hold French debt over German peers to its lowest in over two years, almost to record lows.