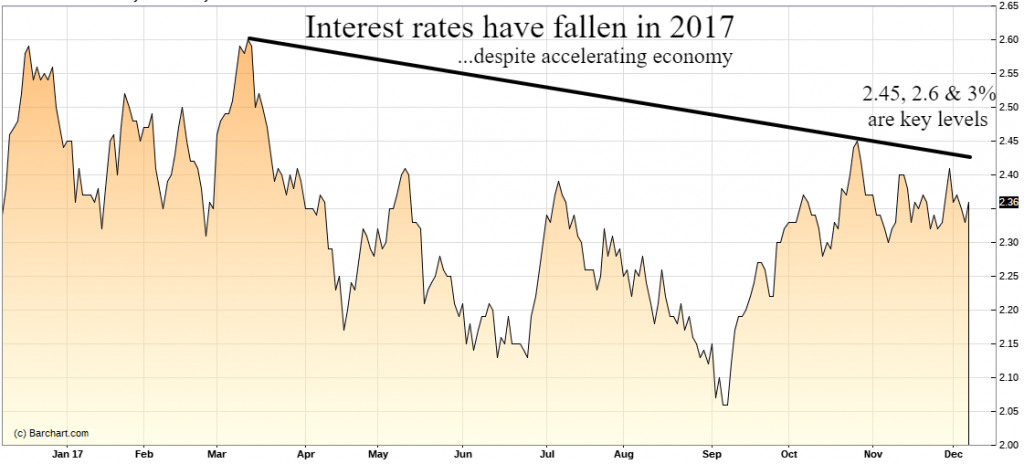

Each year of this enduring slow-growth expansion cycle starting in 2009 has had a growing chorus of doomsayers looking for the next recession. The evidence in forecasting the next economic peak resembles a litany of what if’s to justify a visceral conclusion. Rising interest rates or simply the “feeling†that this expansion is just too darn long are the most popular “reasons†proffered for toil and trouble bubbling around the corner. For years we have heard the sky is falling with regards to the “bond bubbleâ€. Yet interest rates have actually fallen in 2017 despite accelerating economic growth. The yield curve is flattening, yet current yield curve spreads have always been positive for the economy for at least the next 2 years.

(Click on image to enlarge)

The current 8 and a half year long economic expansion is also branded as long in the tooth – a quirky expression emanating from the practice of examining the length of a horse’s tooth to determine its “ageâ€. Just as popular of a caption is the assertion this cycle is in the late innings of the ball game. Since 1945 the average economic growth phase has lasted just under 5 years and the longest expansions in history were the 9 to just under 10-year expansions of the 1960’s and 1990’s. Thus the current growth phase must clearly run out of steam between mid-2018 and early 2019 at the latest, right? Such logic is a bit irrational. Economic cycles don’t have expiration dates and records are eventually broken. What’s more important are the barometers indicating the stage of the economic cycle we are navigating. What’s clear is that from 2009 to early 2017 our economy performed as if in the early to middle innings of a baseball game and only warming up to the middle innings over the past few quarters as the economy moved above-trend growth over 3%. Our assessment was recently echoed by the successful CEO of US Concrete (USCR) who feels we were in the middle innings and with the tax cut have actually reset to the early innings of economic cycle maturation. Further evidence of a new expansion phase can be seen looking at the late 2015 – early 2016 bottom in Oil Prices and Industrial Production (IP) as the global energy recession was winding down.From that mini-recession, Industrial Production growth rates have moved back into positive territory in 2017.