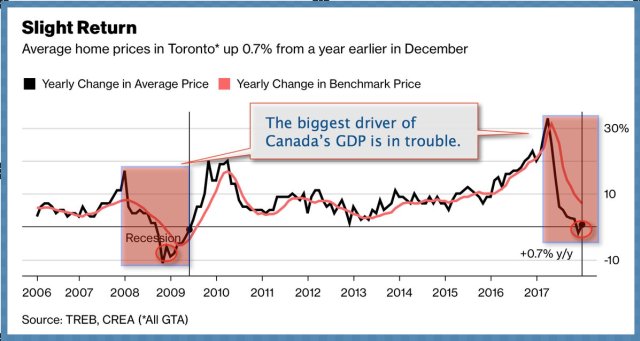

While still up .7% over the last year, Toronto home prices fell for the 7th consecutive month in December, down 8.9% since May–the largest seven-month decline in data tracked since 2000. Falling 3.5% since November, the average sale price in Toronto is still–a wildly un-affordable for most–$735,021 ($1.2 million for single detached homes.) See Toronto home prices fall for seventh month as lending tightens. Here is the chart.

Still with Canadian households at record indebtedness, and new lending restrictions just biting this month, the long overdue slowdown in the real estate sector is barely just started in Canada. The economy which has been precariously dependent on this one sector since at least 2014, wobbles in the balance.Â

As the Bank of Canada frets over consumer debt levels and fantasizes about room for higher rates, this month’s new “stress test†for traditional mortgages is expected to reduce homebuyers’ purchasing power by about 21% (ie., 21% lower prices needed) and disqualify 1 in 10 would-be-borrowers in 2018 and beyond.

Now more levered than Americans before their housing bubble bust in 2006, Canadians are wholly unprepared for a secular downturn in real estate–something not seen in Canada since 1989.

After the average house price in the greater Toronto area (GTA) increased 113% in real terms between 1985 and 1989, the bubble burst. See Toronto housing bubble in 1989:

Coupled with the early 90s recession, a spike in unemployment and a drop in the inflow of immigrants to the area, housing prices in the GTA collapsed. Between 1989 and 1996 average price of a house in GTA have declined by 40% adjusted for inflation…Downtown of Toronto was hit the worst with over 50% decline in value of a home.

Most often missed in these discussions, is that once debt and speculation-fueled financial bubbles burst, it typically takes more than a decade (or two!) for prices to recover their prior peak. By then those who held high, with leverage and low cash liquidity, have long since liquidated low with losses: