Data/Event Risks

- EUR:  For now, all eyes on the Cypriot parliament vote on the deposit levy, scheduled for 16:00 GMT, although it’s unlikely this time will be set in stone. Clearly, the hope is that we see at least some sort of adjustment to exclude deposits below a certain level. If seen, this would be modestly euro positive, but longer-term it’s down to how expectations of contagion are managed and how much other countries believe “this is a one offâ€.

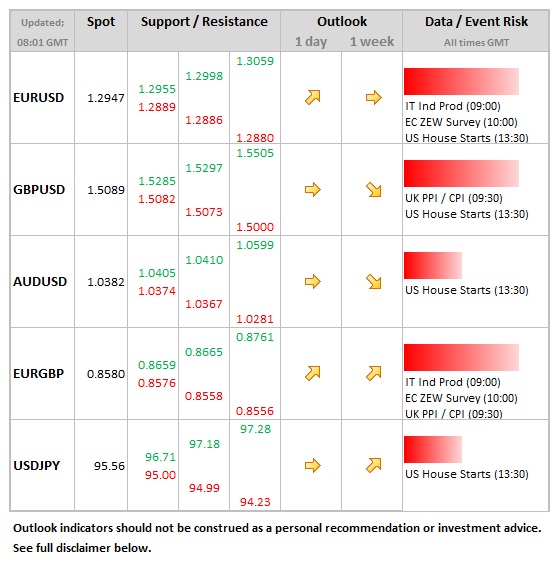

- GBP: Sterling will be sensitive to what happens with CPI data today, where the headline rate is seen rising from 2.7% to 2.8%. There is a growing belief that policy is becoming unhinged, with more QE on the way at the same time that inflation is rising. A higher than expected reading would see sterling weaken, potentially bringing to an end the recent corrective activity seen vs. the USD.

Idea of the Day

The start of the week was all about Cyprus and that’s the way it’s likely to remain for today. After a meeting yesterday, European finance minister appeared open to the idea of sparing smaller savers from the proposed deposit levy, so long as the target EUR 5.8bln was still raised. Despite some of the headlines, the signs were that the fallout from Cyprus beyond its shores was relatively contained, at least in terms of financial markets.

Italian and Spanish bond yields moved 5-10bp wider over Germany on the day, whilst German 2 year yields briefly touched negative territory, a level which has not been reached since the dying days of last year. Institutional volumes were on the light side, suggesting that there was no large scale unwinding of positions by larger players. The euro would gain on a vote that passes the levy, moreso if smaller savers are spared. Even if contagion is contained, the political damage for the EU will remain, as well as residual fears in the periphery that this may not be a “one offâ€, despite the reassurances to the contrary.

Latest FX News

- EUR: The price action on Monday was reflecting a market that was nervous regarding the situation in Cyprus, but not running scared. This was evident in the recovery seen after the early Asia losses, together with the fact that institutional volumes were in line with the recent norm.

- JPY:  The yen was generally weaker overnight, with USDJPY rising to just above 95.50. BoJ governor Shirakawa stepped down today, with incoming Kuroda bringing in expectations of more aggressive easing policies from the central bank.

- AUD: Pretty steady, with the latest minutes from the RBA underlining the view that rates are on hold for the moment, with the higher currency and savings allowing rates to remain low. This was pretty much priced in, so AUD was steady, but in the bigger picture, the Aussie continued to perform well.

Further:Â Dollar Enjoys Cypriot Crisis