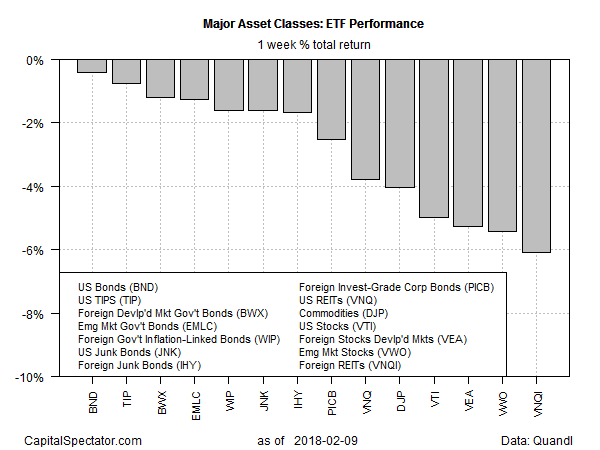

Red ink continued to spill across all the major asset classes last week, based on a set of exchange-traded products. The declines mark the second straight week of across-the-board selling.

The biggest setback was in foreign real estate/REITs. Vanguard Global ex-US Real Estate (VNQI) suffered a sharp 6.1% decline over the five trading days through Feb. 9, settling at its lowest close in two months.

The lightest tumble was posted by US investment-grade bonds. Vanguard Total Bond Market (BND) dipped a relatively soft 0.4%. Although BND’s latest decline is mild, the ETF ended last week at its lowest level since May 2017, based on adjusted prices that factor in distributions.

The recent rise in Treasury yields, driven by expectations of higher inflation, is weighing on fixed-income securities generally. The slide in bond prices is unusual at a time of falling stock markets, but there’s a macro explanation, notes Robin Griffiths, chief technical strategist at ECU Group.

“In normal rotation from bull to bear, you’d go straight into government bonds, but this is the problem. With interest rates going up, because the economy is strong and inflation is picking up, government bonds have become not the safest asset class in the planet but toxic waste,†he said on CNBC today. “So, by relative comparison you’re sort of trapped into equities even though you know they are not good value.â€

Â

Despite the recent market turmoil, the one-year trend summary continues to reflect an upside bias in most corners. Although returns have been trimmed lately, broadly defined equity markets continue to post solid gains, led by emerging markets.

Vanguard FTSE Emerging Markets (VWO) continues to hold the top spot for the major asset classes for one-year performance, posting a 21.3% total return through last week’s close.

Losses in the one-year column are currently limited to a handful of markets, with US real estate investment trusts sliding the most vs. the year-earlier level. Vanguard REIT (VNQ) is off 7.0% for the year through Feb. 9.