Idea of the Day

The yen continues to be the big standout on the charts. As a debt deal in the US was looking more likely yesterday, the yen was a one-way street lower, both vs. the USD and EUR, pulling USDJPY away from the 200-day moving average which it had threatened to break below earlier in the week. We’ve said before that the reason for being bearish on the yen have been a lot weaker of late, in part allowing it to trade more like the safe haven currency of old. It’s still likely to be dollar yen where the main impact of a resolution of the current budget and debt crisis in the US is felt, because it was the biggest moving against the dollar when the dollar was weakening and has proved so again in the subsequent dollar recovery. But what is emerging out of Washington is just a sticking plaster on the debt ceiling. Some tough negotiations are going to be felt over the coming weeks and at present it’s difficult to see how long-term viable solutions are going to emerge from it.

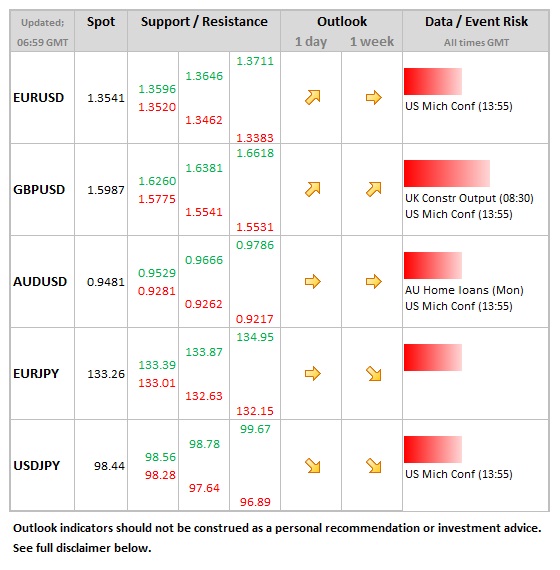

Data/Event Risks

USD: Just Michigan confidence data at the end of the week, against which the dollar could be more sensitive on the basis of the lack of data from official government sources at the moment.

AUD:Â Housing market data is released on Monday, with home loans seen falling 1.3% after 2.4% gain in July. Aussie could struggle to gain after recent limited reaction to stronger jobs data earlier in the week.

Latest FX News

JPY:Â USDJPY feeling a little more confident now that the 200-day moving average remained intact on a closing basis. Yen weaker for the fourth consecutive day as temporary resolution to US debt deal looks closer.

AUD:Â Feeling a little tired in the legs, as the reaction to the jobs data earlier in the week showed, but weaker US dollar environment allowing push back up towards the 0.9500 area.

GBP:Â Struggling to regain its footing below the 1.60 area against the dollar after the weaker than expected IP data see earlier in the week.

Further reading:

yen

debt crisis