Idea of the Day

We start moving on from the US shutdown and debt ceiling as US data starts to come through (employment report released tomorrow). As the weekly claims data has illustrated, a lot of data could well be distorted by the events of recent weeks, making it more difficult to read the underlying tone of the economy. Suggestions are that around 0.5% could have been knocked off growth in the current quarter, losses which may be hard to get back in the next quarter if the uncertainty continues. We outlined what we thought this meant for the dollar last week, with the delay of tapering and continued uncertainty making it more difficult for the dollar to push to the upside. The delay of data will also likely not be supportive of a stronger dollar tone.

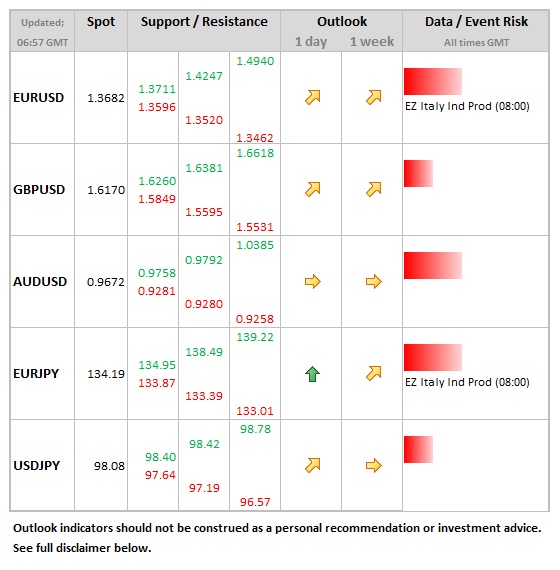

Data/Event Risks

EUR:Â Just production orders data from Italy scheduled, which is not a major issue for the single currency unless significantly out of line against light volumes.

USD:Â Existing home sales data is seen falling 3.3% in September, after 1.7% rise in August. The market has been starved of US data recently, so could be that it is more sensitive than usual to stronger or weaker data.

Latest FX News

JPY:Â Export growth fell short of expectations, with trade balance coming out at JPY 932bln. The yen was weaker on the news, USDJPY rising above 98.00 in a move that was largely sustained over the Asia session.

AUD: The upside momentum to the Aussie appears to be waning, with a new high for the month made overnight just 1 pip higher vs. Friday’s level.

USD: After the post-deal sell-off, it’s interesting to note that the weakness has been sustained, especially against the Aussie. This suggests a more fundamental shift in attitudes towards the dollar in the wake of recent events. The dollar stands just above an 8 month lows on the dollar index.

Further reading:

EUR/USD Oct. 18 – Surging Euro Hits Eight-Month Highs

Forex Analysis: EUR/USD Achieves 1.3700 Upside Target