The focus is on sterling with inflation data released today. Data last month showed the headline rate falling to the lowest rate in just over a year, this at a time when the economy has been outperforming. But this was owing to changes in fuel and also education, which tend to not be related to the pace of activity in the wider economy.

This was also one of the biggest surprise inflation numbers for this year, as normally inflation has tended to come into line with expectations, after a strong period during latest 2010 and early 2011 during which it continually surprised to the upside. It can be better to watch the ‘core’ rate during period of headline volatility, which excludes fuel, food and other volatile items.

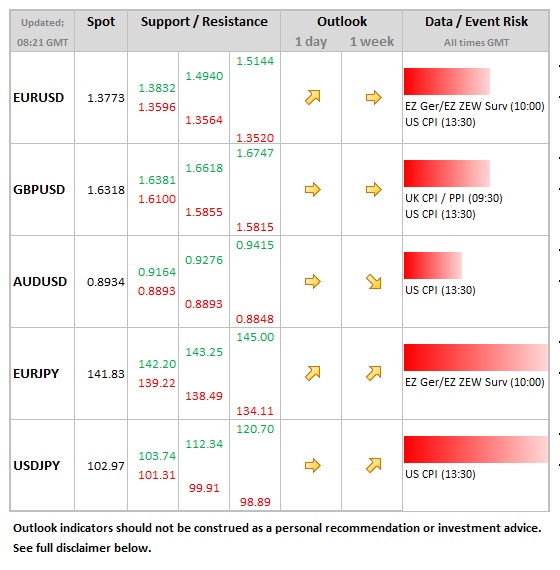

This is expected to nudge higher to 1.8% (from 1.7%), this being the lowest level for over four years. Sterling feels more vulnerable to a weaker number, given that it has lagged other currencies vs. the dollar so far this month, cable once again having retreated from the recent highs above the 1.64 level.

Update: CPI came out at 2.1% and core CPI at 1.8%.

Latest FX News

EUR: Data yesterday from the ECB showed that banks are still repaying loans back to the ECB ahead of year end and this has seen money market rates squeeze further higher. But this was the last opportunity for banks to repay until the middle of January, so whilst rates remain high, they should not squeeze much higher from here. This could mean further euro strength limited from here.

AUD:  No great surprises in the latest RBA minutes, which showed that the board saw the Aussie as “uncomfortably high†but were not yet prepared to close off the possibility of reducing rates further. The Aussie was a little choppy, but was ultimately unmoved by the release.

USD:  The dollar finds itself near the lows of the past 6 weeks, even though the odds of tapering this week are more finely balanced that before (largely owing to euro developments). Firmer than expected industrial production yesterday also helped at the margin.

Data/Event Risks

GBP:  There was a chunky drop in inflation in last month’s data, from 2.7% to 2.2% on an annual basis. It was changes in tuition fees and also petrol that pulled down the rate, so the market is expecting it to retain this lower level at 2.2%. Higher number would offer more support to sterling.

USD: The CPI data is the initial focus for the dollar, with headline prices seeing rising to 1.3%, whilst the core rate holds steady at 1.7%. The two day FOMC meeting begins today, but results are not due until later on tomorrow.

More:

- Will tapering begin on Wednesday?

- 40% of QE tapering in December