Image Source:

Image Source:

Earlier today we wrote an extensive preview of what to expect from Nvidia’s Q3 earnings (), but for those who missed it here is the summary: sky high expectations, which only go higher in 2025 and beyond when the full rollout of Blackwell is expected to hit the P&L, with everyone already long (Goldman desk positioning is 9 out of 10) and anything less than perfection will be punished by the market. The bull/bear case according to Goldman is as follows:

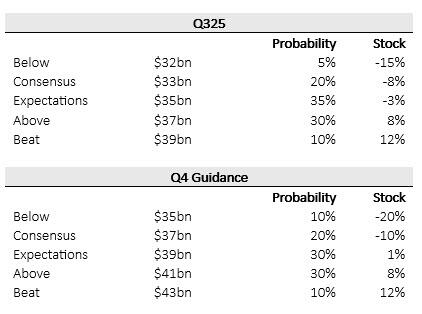

In terms of expectations, Q3 revenue is projected to come in at $33.25 billion, the average estimate of analysts; and the median Q4 revenue target is $37.1 billion. Keep in mind that that number has moved around a lot in the past few days as analysts have made last-minute tweaks to their models. While the current high sales estimate for the third quarter is $41.2 billion, but some investors have told me that the ‘whisper number’ may be above thatBeyond the headlines, JPM says that the key near-term bogeys are the following:

Other things to look out for when the company starts speaking will include how much supply it’s getting from its manufacturing partners. Like most chipmakers, Nvidia outsources production. Taiwan Semiconductor is the best in the business, and Nvidia’s pace of growth heavily depends on how well TSMC is able to provide Nvidia with the capacity it needs.Amusingly, Nvidia shares actually closed down today, though far from session lows, ahead of the earnings report. Still, shares are up nearly 200% so far this year, and one of the best performers on the S&P 500 Index. Nvidia’s market cap north of $3.6 trillion makes it the biggest weighting in the S&P 500, meaning that any move in the stock could swing the entire market.With that in mind, here is what NVDA reported moments ago:

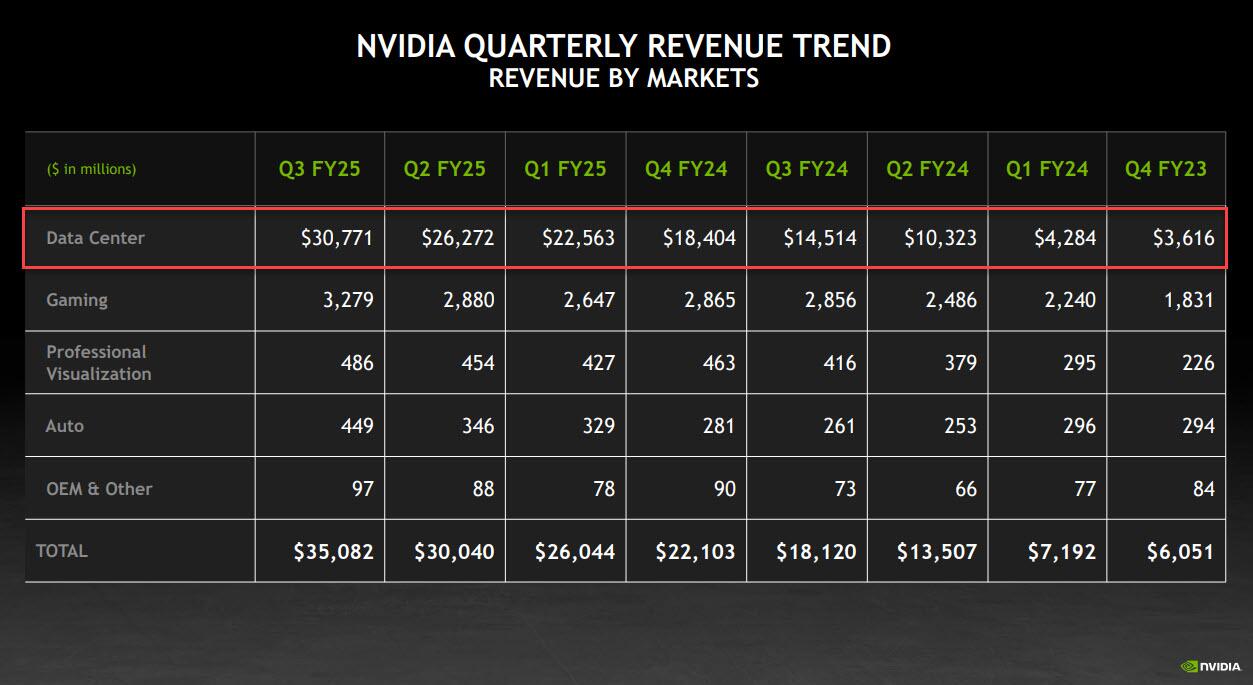

- Data center revenue $30.8 billion vs. $14.51 billion y/y, beating estimates of $29.14 billion

- Gaming revenue $3.3 billion, +15% y/y, beating estimates of $3.06 billion

- Professional Visualization revenue $486 million, +17% y/y, beating estimates of $477.7 million

- Automotive revenue $449 million, +72% y/y, beating estimates of $364.5 million

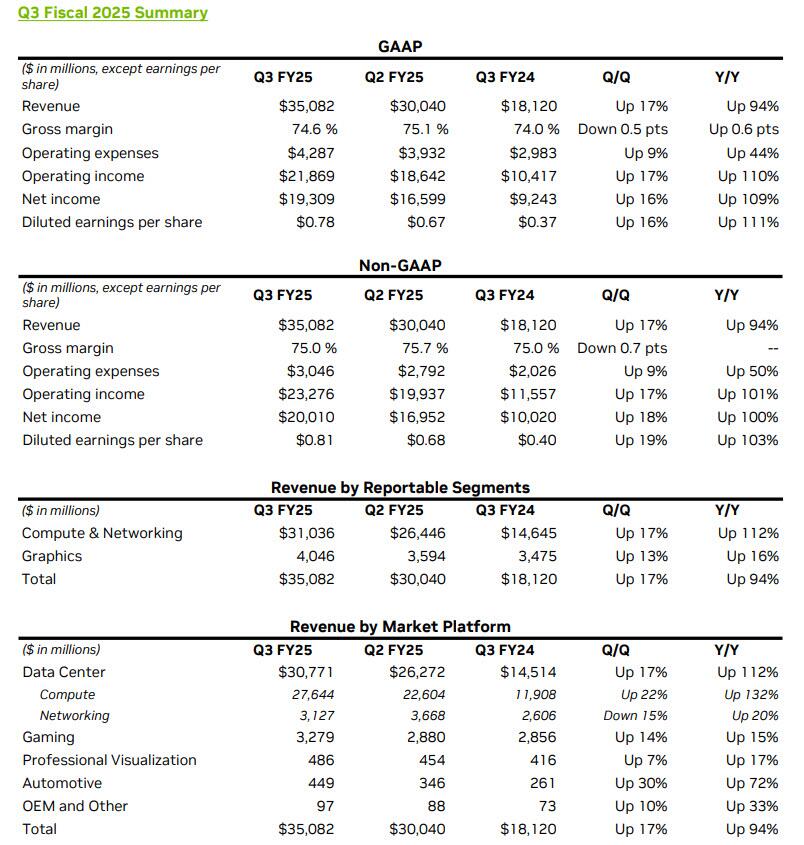

- Adjusted operating expenses $3.05 billion, +50% y/y, beating estimates of $2.99 billion

- Adjusted operating income $23.28 billion vs. $11.56 billion y/y, beating estimates of $21.9 billion

The revenue trend, as expected, is impressive especially at the Data Center level where all the growth is.(Click on image to enlarge)

Here is a full breakdown of recent results:(Click on image to enlarge) But while the Q3 results were stellar, the company’s guidance came in on the weak side of the buyside expectations we discussed in our premium preview.

But while the Q3 results were stellar, the company’s guidance came in on the weak side of the buyside expectations we discussed in our premium preview.

Oops: while this was above the median consensus of $37.1BN, it was far below the buyside expectations of $38.8BN; It was also well below and close to where the bank saw the stock dropping -10%. In fact, some estimates for Q4 revenue were as high as $41 billion!

The rest of the guidance was in line but far less important:

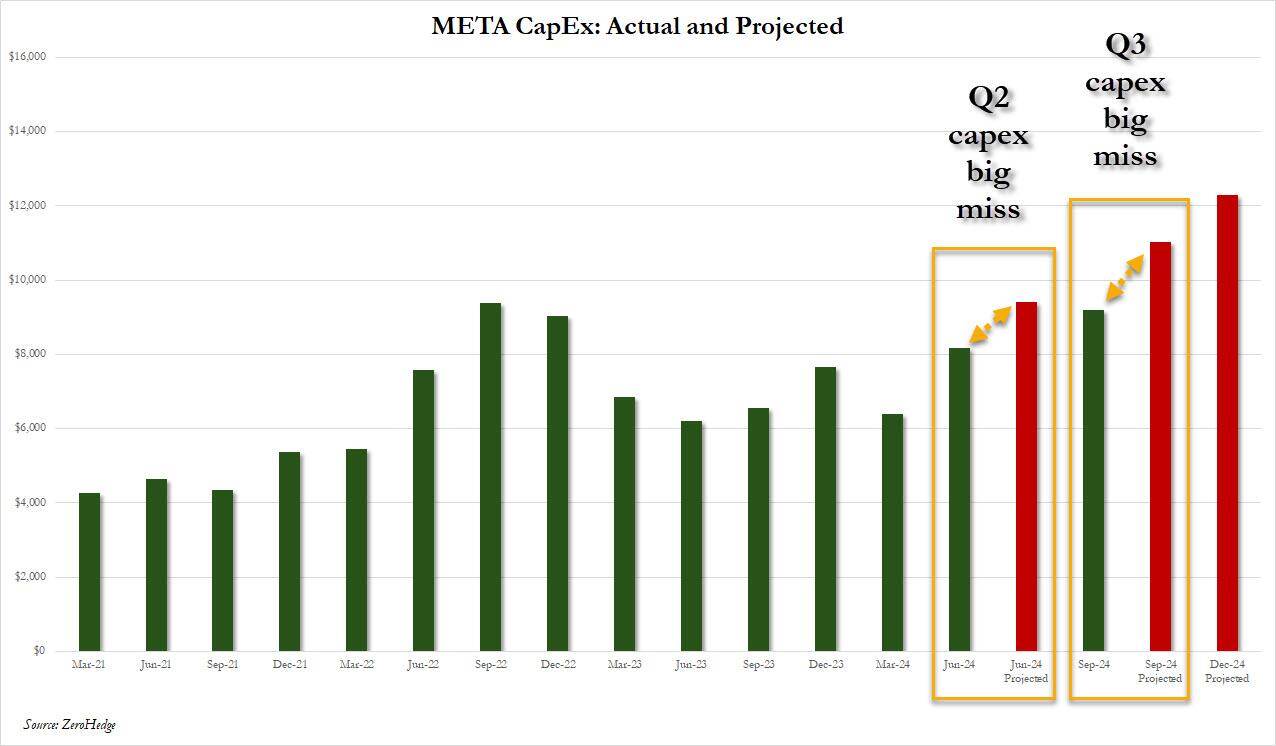

Nvidia has only missed analysts’ estimates on quarterly revenue once in the past five years. And it has exceeded expectations by as much as 20% in recent periods, creating a very high bar for its performance.The muted outlook suggests that AI excitement may be getting ahead of reality according to Bloomberg. Nvidia investors had bid up the shares nearly 200% in 2024, turning it into the world’s most valuable company at $3.6 trillion in market cap. But the chipmaker has had trouble keeping up with demand for its products and struggled with production snags this year.To be fair, even with the disappointing outlook, Nvidia’s growth over the past two years has been staggering, simply because not one chipmaker has been able to take its market share (Intel unprecedented collapse in recent years can be largely to blame for that). Its sales are poised to double for a second year in a row, and it now notches more money in profit than it used to generate in total revenue (thanks to that 75% profit margin).Nvidia’s data center division alone now has more revenue than its two nearest rivals, Intel and AMD combined. Net income this year is on course to exceed revenue at Intel, a company that was the chip industry’s titan for decades.The company’s biggest moneymaker is its accelerator chip, which helps develop AI models by bombarding them with data. Since OpenAI’s ChatGPT chatbot debuted in 2022, a frenzy of artificial intelligence services has created insatiable demand for the product.Other recent earnings reports have given strong signals for AI. Major Nvidia customers, including Microsoft, Amazon’s AWS and Meta have reaffirmed their commitment to spend on AI infrastructure, even if few have actually done the spend, as we noted .(Click on image to enlarge) Nvidia hopes to stay ahead of rivals by accelerating its pace of innovation. That includes a commitment to updating its lineup annually; the company is currently introducing a design called Blackwell, which is faster and has an improved ability to link up with other chips, and which is expected to hit the company’s P&L early next year, as a bevy of manufacturing challenges have slowed the Blackwell rollout. For now, Nvidia can’t fill all the orders it’s receiving, the company has said. After production improves, supplies will be plentiful, according to CEO Jensen Huang. For his sake, hopefully by then no competitors will have been able to come out with a faster, cheaper chip.The Santa Clara, CA-based company has rapidly expanded its product lineup to include networking, software and services, as well as fully built-out computer systems. Huang is traveling the world lobbying for a broader adoption of his technology and trying to spread its use by corporations and government agencies.Shares of Nvidia fell as much as 5% in after hours trading following the announcement, before settling about 2% lower, far below the 8.8% straddle. They previously closed at $145.89 in New York.(Click on image to enlarge)

Nvidia hopes to stay ahead of rivals by accelerating its pace of innovation. That includes a commitment to updating its lineup annually; the company is currently introducing a design called Blackwell, which is faster and has an improved ability to link up with other chips, and which is expected to hit the company’s P&L early next year, as a bevy of manufacturing challenges have slowed the Blackwell rollout. For now, Nvidia can’t fill all the orders it’s receiving, the company has said. After production improves, supplies will be plentiful, according to CEO Jensen Huang. For his sake, hopefully by then no competitors will have been able to come out with a faster, cheaper chip.The Santa Clara, CA-based company has rapidly expanded its product lineup to include networking, software and services, as well as fully built-out computer systems. Huang is traveling the world lobbying for a broader adoption of his technology and trying to spread its use by corporations and government agencies.Shares of Nvidia fell as much as 5% in after hours trading following the announcement, before settling about 2% lower, far below the 8.8% straddle. They previously closed at $145.89 in New York.(Click on image to enlarge) More By This Author:

More By This Author: