Image source: After elevated inflation prints and mildly hawkish commentary from Fed Chair Powell this week, a set of decent retail sales numbers, but admittedly mixed manufacturing numbers leaves the prospect of a December Fed rate cut firmly in the balance. The jobs report will be key on 6 December and for now we are sticking with the view that a cut is more likely than not.

Image source: After elevated inflation prints and mildly hawkish commentary from Fed Chair Powell this week, a set of decent retail sales numbers, but admittedly mixed manufacturing numbers leaves the prospect of a December Fed rate cut firmly in the balance. The jobs report will be key on 6 December and for now we are sticking with the view that a cut is more likely than not.

Consumers just keep on spending

US retail sales rose 0.4% month-on-month in October, a touch higher than the consensus 0.3% MoM expectation while September’s growth rate was revised up to 0.8% from 0.4%. A big 1.6% MoM increase in autos was the main factor, but building materials (+0.5%) and restaurants and bars (+0.7%) both contributed strongly.The “control” group, which excludes volatile items (the three just listed plus gasoline) and has a better record of tracking broader consumer spending that includes services, was quite a bit weaker, falling 0.1% MoM versus a +0.3% consensus. However, September’s growth rate was revised up to +1.2% from +0.7%. The key weakness was in furniture (-1.3%), health & personal care (-1.1%), sporting goods (-1.1%) and miscellaneous (-1.6%). All other components were in a -0.2% to +0.3% range.It is likely that hurricane effects and warm weather across the US have had an impact on this report by boosting eating and drinking venues and hurting furniture and clothing stores, but the underlying trend remains firm.

The path of the jobs market will determine if we see a slowdown

In that regard we know the top 20% of households by income spend more than the entirety of the lowest 60% of households by income and the top 20% are in fantastic financial shape. Inflation has been less of a constraint, property and equity market wealth has soared and high interest rates benefit them – receiving 5%+ on money markets versus perhaps paying 3.5% on a mortgage, if they have one.However, it is a very different story for the lowest 60% by income with inflation being much more painful while wealth gains have been far more modest, and soaring car loan and credit card borrowing costs have hurt. Loan delinquencies are on the rise and the proportion of credit card holders only making the minimum monthly payments has been soaring. That’s what makes the jobs data so important – if we see continued cooling there it increases financial stress and that could prompt weakness ahead even if the top 20% keep on spending strongly.For now though the data is in line with Fed Chair Powell’s commentary that the “economy is not sending signals that we need to be in a hurry to lower rates” and leaves the market pricing just 15bp of a potential 25bp rate cut at the December FOMC meeting. Next week’s calendar is light and in the knowledge that the core PCE deflator is almost certainly going to come in at 0.3% MoM on 27 November, and the jobs report on 6 December is going to be the next big focus for markets.

Manufacturing held back by strikes and storms, but has sentiment been boosted by Trump’s victory?

Industrial production fell 0.3% in October, not quite as soft as the -0.4% expectation in the market, but September’s output was revised down to -0.5% from -0.3%. Manufacturing output fell 0.5% in October as expected. The Boeing strike clearly weighed with output down 13.9% MoM for transportation after a 14.9% MoM drop in September. This should rebound markedly in coming months. Auto production also fell for the second month in a row with a mixed performance from other sectors. It is certainly likely that recent hurricanes disrupted output on a regional level – the Federal Reserve estimates the strikes knocked 0.2 percentage points off industrial production growth while the hurricanes subtracted a further 0.1pp. Nonetheless, that still points to a contraction even after those factors are excluded. Utilities output rose 0.7% while mining rose 0.3%.

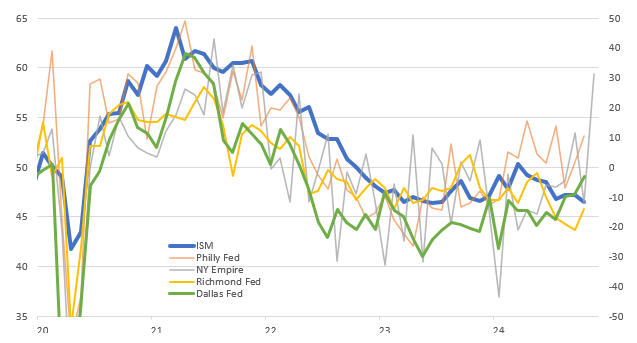

US manufacturing surveys

Source: Macrobond, ING Meanwhile, the NY Fed regional Empire manufacturing survey surged from -11.9 to +31.2. The consensus was 0.0. Now a lot of caution is needed on this report. The NY Fed area is a relatively small region for manufacturing when compared to the MidWest but this is a very big swing. It implies the level of activity is close to the situation we found ourselves at the height of the rebound of the economy in 2021. That said it is a measure or perception of general business conditions and the responses largely came in just after the election outcome – so the prospect of tax cuts and the belief in some circles that tariffs could boost the manufacturing sector may be in play here, but to be fair new orders performed strongly even if other areas remained subdued. We will have to see what the Philadelphia Fed, Kansas Fed and Dallas Fed surveys say next week. If the ISM was to rebound too that would increase the pressure on the Fed to slow the pace of rate cuts.More By This Author:

Source: Macrobond, ING Meanwhile, the NY Fed regional Empire manufacturing survey surged from -11.9 to +31.2. The consensus was 0.0. Now a lot of caution is needed on this report. The NY Fed area is a relatively small region for manufacturing when compared to the MidWest but this is a very big swing. It implies the level of activity is close to the situation we found ourselves at the height of the rebound of the economy in 2021. That said it is a measure or perception of general business conditions and the responses largely came in just after the election outcome – so the prospect of tax cuts and the belief in some circles that tariffs could boost the manufacturing sector may be in play here, but to be fair new orders performed strongly even if other areas remained subdued. We will have to see what the Philadelphia Fed, Kansas Fed and Dallas Fed surveys say next week. If the ISM was to rebound too that would increase the pressure on the Fed to slow the pace of rate cuts.More By This Author:

Decent US Trends Leaves December Rate Cut Chances In The Balance