Goldman extended the banks’ solid results this morning when it reported a 45% jump in profit to $3bn in the third quarter, boosted by its equity trading business, while beating solidly on revenues even as the investment bank took another hit from its retreat from retail banking. Goldman’s net income of $2.99bn compared with $2.1bn in the third quarter of last year and outstripped analysts’ estimates of about $2.5bn. Here are the details for Q3:

- FICC Sales & Trading Revenue $2.96 billion, beating estimates of $2.96 billion

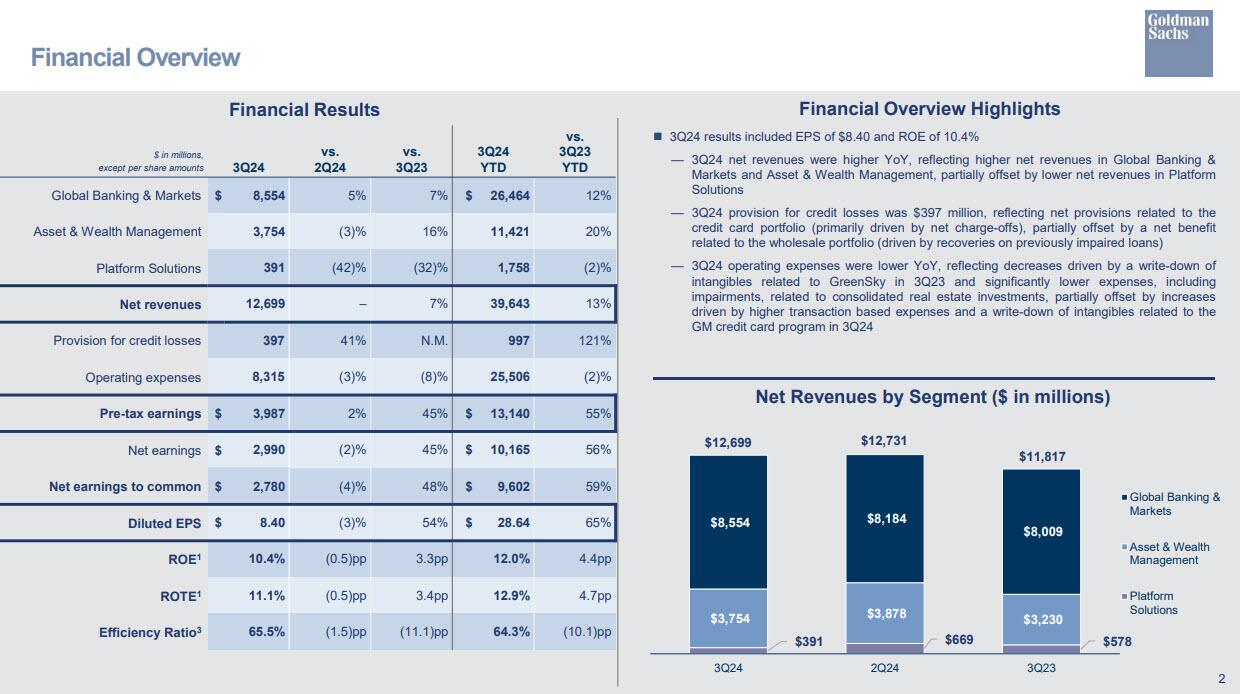

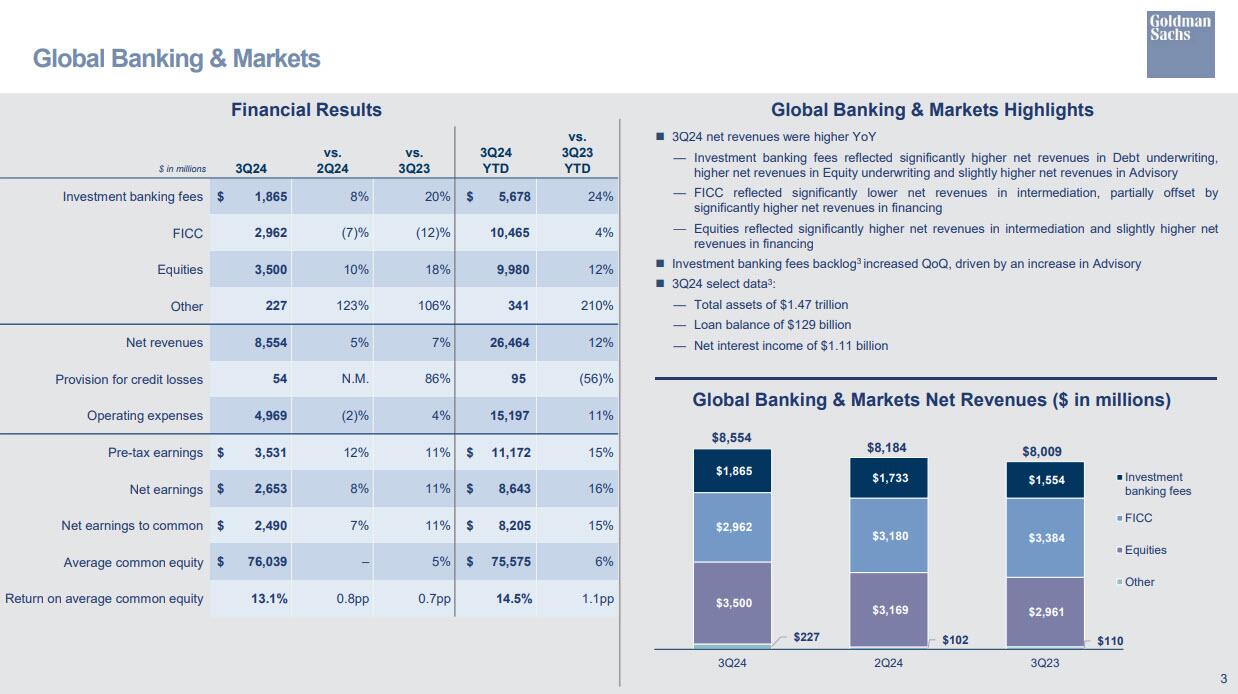

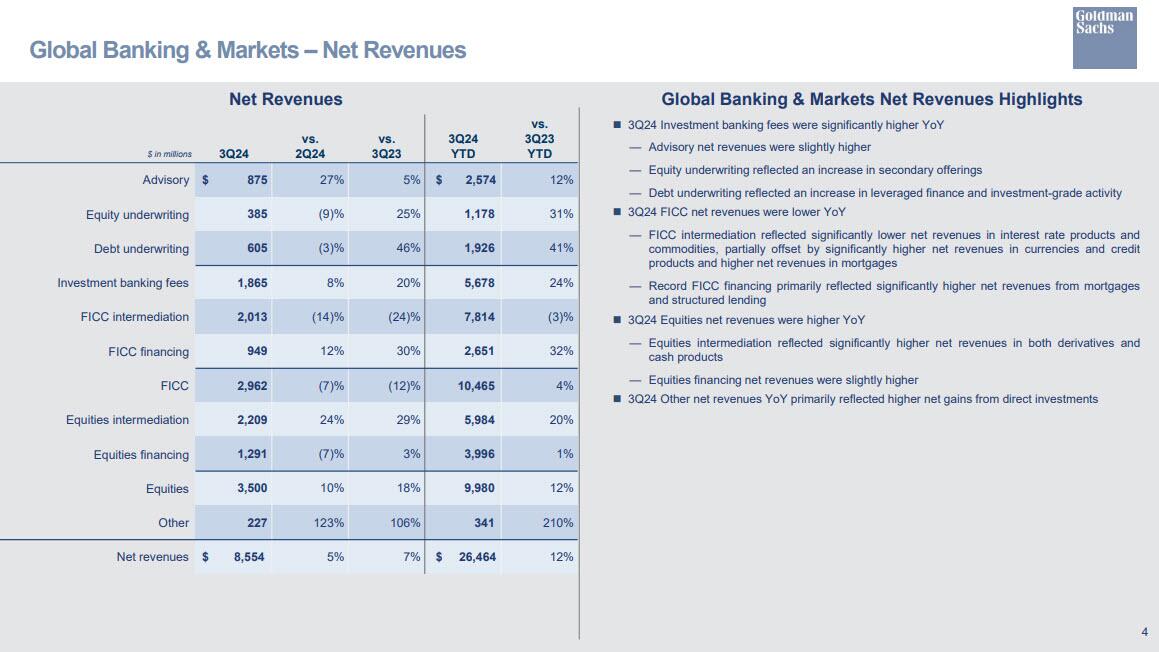

- Global Banking & Markets net revenues $8.55 billion, +6.8% y/y, beating estimates of$7.65 billion

- Investment banking revenue $1.86 billion, +20% y/y, beating estimates of $1.68 billion

- Equities sales & trading revenue $3.50 billion, +18% y/y, beating estimates of $2.95 billion

- Advisory revenue $875 million, +5.3% y/y, beating estimates of $757.5 million

- Equity underwriting rev. $385 million, +25% y/y, beating estimates of $359.6 million

- Debt underwriting rev. $605 million, +46% y/y, beating estimates of $567.9 million

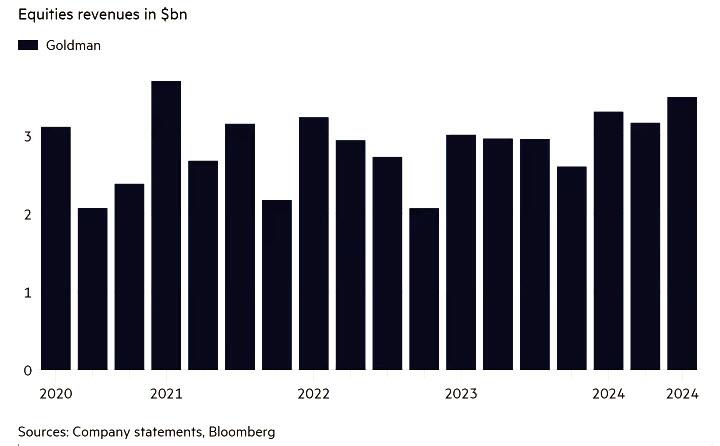

(Click on image to enlarge) In the best quarter for Goldman’s stock trading business since the start of 2021 – and on track for its best year ever – equity trading revenues reached $3.5bn, up 18% and defying expectations of a flat quarter. The firm credited significantly higher intermediation revenue in derivative and cash products.(Click on image to enlarge)

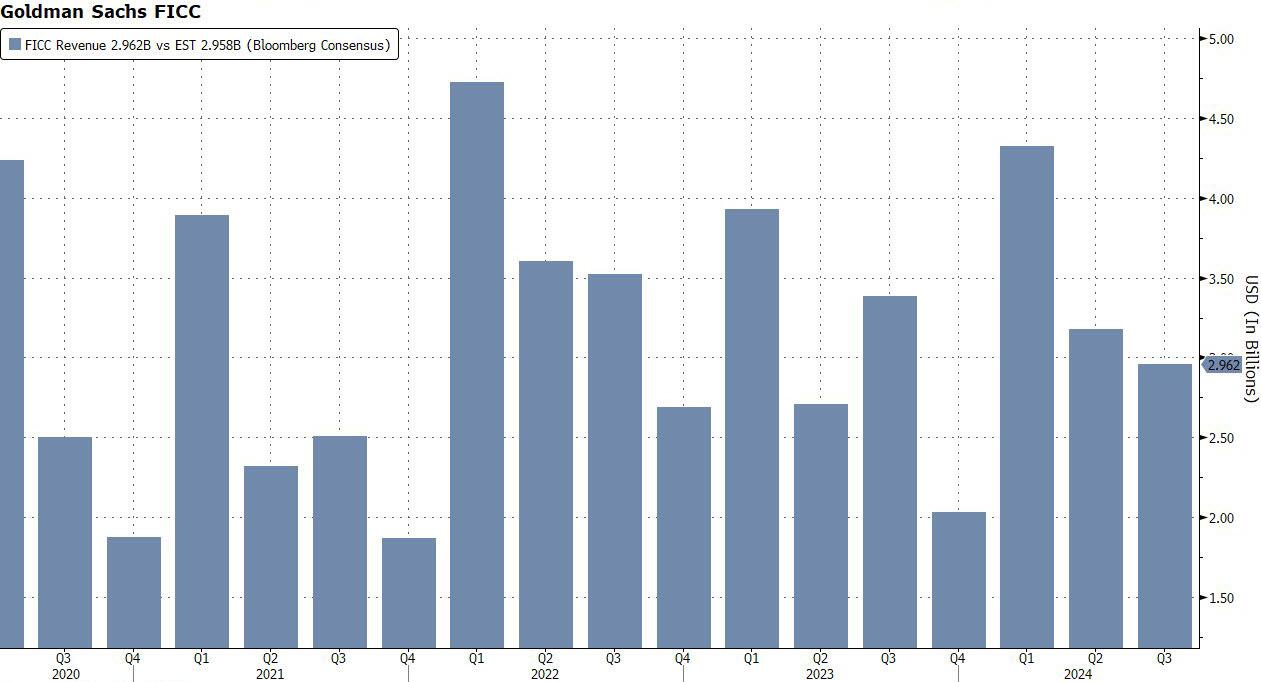

In the best quarter for Goldman’s stock trading business since the start of 2021 – and on track for its best year ever – equity trading revenues reached $3.5bn, up 18% and defying expectations of a flat quarter. The firm credited significantly higher intermediation revenue in derivative and cash products.(Click on image to enlarge) On the other hand, the company’s biggest profit center, fixed income trading (FICC) revenues fell 12% to $2.96bn, in line with estimates; Goldman said lower FICC revenues “reflecting significantly lower net revenues in FICC intermediation, due to significantly lower net revenues in interest rate products and commodities, partially offset by significantly higher net revenues in currencies and credit products and higher net revenues in mortgages.”(Click on image to enlarge)

On the other hand, the company’s biggest profit center, fixed income trading (FICC) revenues fell 12% to $2.96bn, in line with estimates; Goldman said lower FICC revenues “reflecting significantly lower net revenues in FICC intermediation, due to significantly lower net revenues in interest rate products and commodities, partially offset by significantly higher net revenues in currencies and credit products and higher net revenues in mortgages.”(Click on image to enlarge) In August, the bank said the co-head of its commodities business, Qin Xiao, was leaving after just a few months in the role at a time when gains in that business have slowed. CEO David Solomon last month flagged a significant slowdown in revenue tied to equity and debt investments in its money-management unit, particularly as the bank pares back investing from its balance sheet. That revenue was $294 million, a sharp slowdown from recent quarters, including the more than $1.2 billion at the end of last year.(Click on image to enlarge)

In August, the bank said the co-head of its commodities business, Qin Xiao, was leaving after just a few months in the role at a time when gains in that business have slowed. CEO David Solomon last month flagged a significant slowdown in revenue tied to equity and debt investments in its money-management unit, particularly as the bank pares back investing from its balance sheet. That revenue was $294 million, a sharp slowdown from recent quarters, including the more than $1.2 billion at the end of last year.(Click on image to enlarge) Some more results:

Some more results:

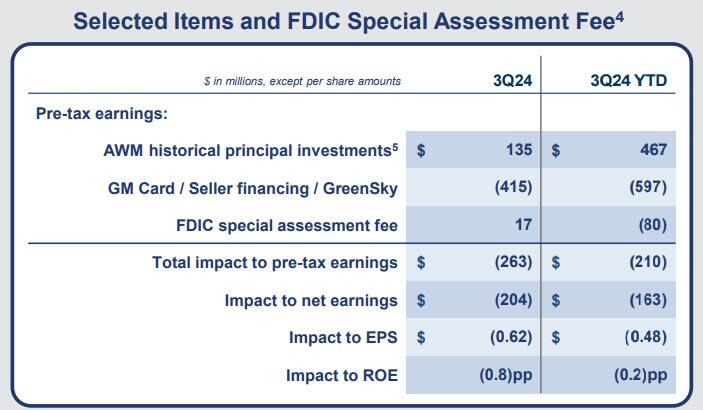

Despite the narrowed focus in its business, now that it has jettisoned its ill-fated consumer banking foray, the bank is still shy of its mid-teens return-on-equity target, having only hit that mark once in the past 10 quarters. In the three months through September, the New York-based firm posted a 10.4% ROE — a measure that tracks how profitably the bank invests shareholder equity.Goldman’s results would have been even stronger were it not for a charge due to losses Goldman took a year ago tied to its pullback from consumer banking and writedowns on real estate investments. The bank’s results included a $415 million hit tied to severing the firm’s credit-card partnership with General Motors and jettisoning other small retail ventures. Barclays Plc said Monday it’s taking over the GM business after Goldman fumbled its foray into consumer lending. The Wall Street firm has spent much of the last year trying to drop its much bigger card tie-up with Apple. That book of business, which has about $17 billion in outstanding balances, could suffer a steeper hit if Goldman exits the partnership by selling the loans at a discount.Goldman also benefited from a revival of dealmaking activity in what Wall Street hopes is the start of a sustained recovery. Investment banking fees rose 20% at $1.865bn, ahead of the $1.68bn estimates. Merger-advisory fees were $875 million. Goldman jumped out in front of JPMorgan on that metric after falling behind its rival in the second quarter. Its equity-underwriting business posted revenue of $385 million and debt-underwriting revenue was $605 million. Also of note: the bank said that the backlog of investment banking fees was up from the end of the second quarter “and the end of 2023.”(Click on image to enlarge)

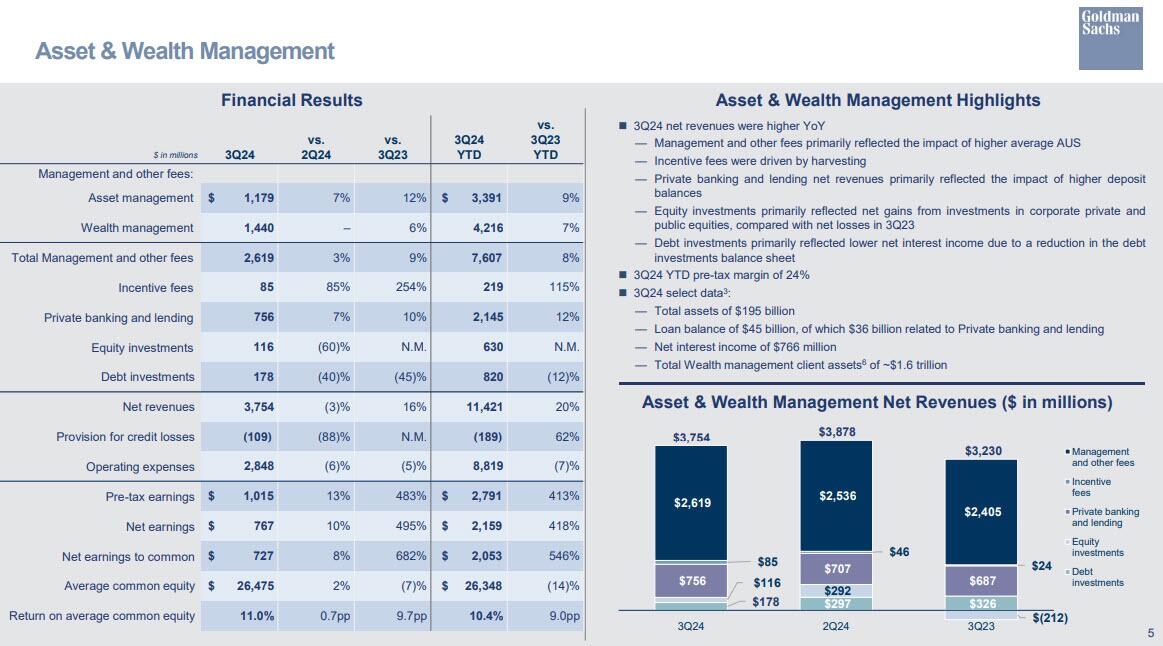

The Wall Street firm has spent much of the last year trying to drop its much bigger card tie-up with Apple. That book of business, which has about $17 billion in outstanding balances, could suffer a steeper hit if Goldman exits the partnership by selling the loans at a discount.Goldman also benefited from a revival of dealmaking activity in what Wall Street hopes is the start of a sustained recovery. Investment banking fees rose 20% at $1.865bn, ahead of the $1.68bn estimates. Merger-advisory fees were $875 million. Goldman jumped out in front of JPMorgan on that metric after falling behind its rival in the second quarter. Its equity-underwriting business posted revenue of $385 million and debt-underwriting revenue was $605 million. Also of note: the bank said that the backlog of investment banking fees was up from the end of the second quarter “and the end of 2023.”(Click on image to enlarge) Goldman’s asset and wealth management division, which is central to Solomon’s efforts to make the bank less reliant on investment banking and trading, reported a 16% increase in revenues to $3.754 bn. Management fees climbed 9%. The bank reported $16 billion of fundraising in the alternatives business, mostly tied to credit-related strategies. Here is the full breakdown:

Goldman’s asset and wealth management division, which is central to Solomon’s efforts to make the bank less reliant on investment banking and trading, reported a 16% increase in revenues to $3.754 bn. Management fees climbed 9%. The bank reported $16 billion of fundraising in the alternatives business, mostly tied to credit-related strategies. Here is the full breakdown:

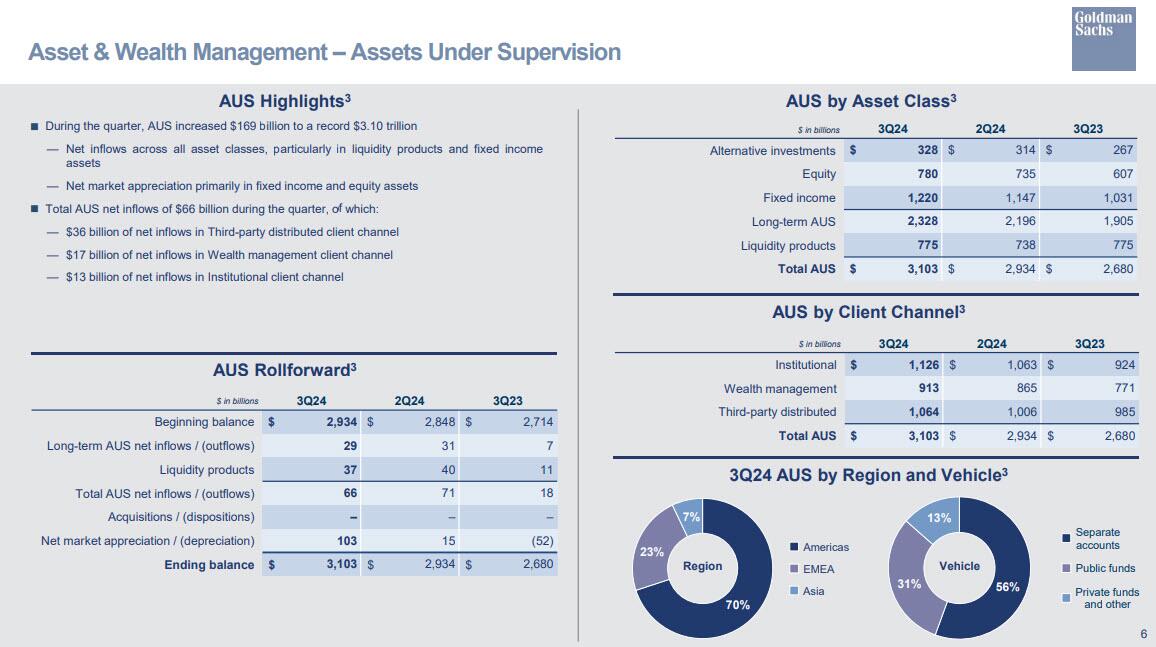

(Click on image to enlarge) Total assets under supervision for Goldman’s wealth management group rose $169 billion to a record $3.10 trillion, driven by inflows across all asset classes, particularly in liquidity products and fixed income assets. The group also benefited from net market appreciation primarily in fixed income and equity assets.(Click on image to enlarge)

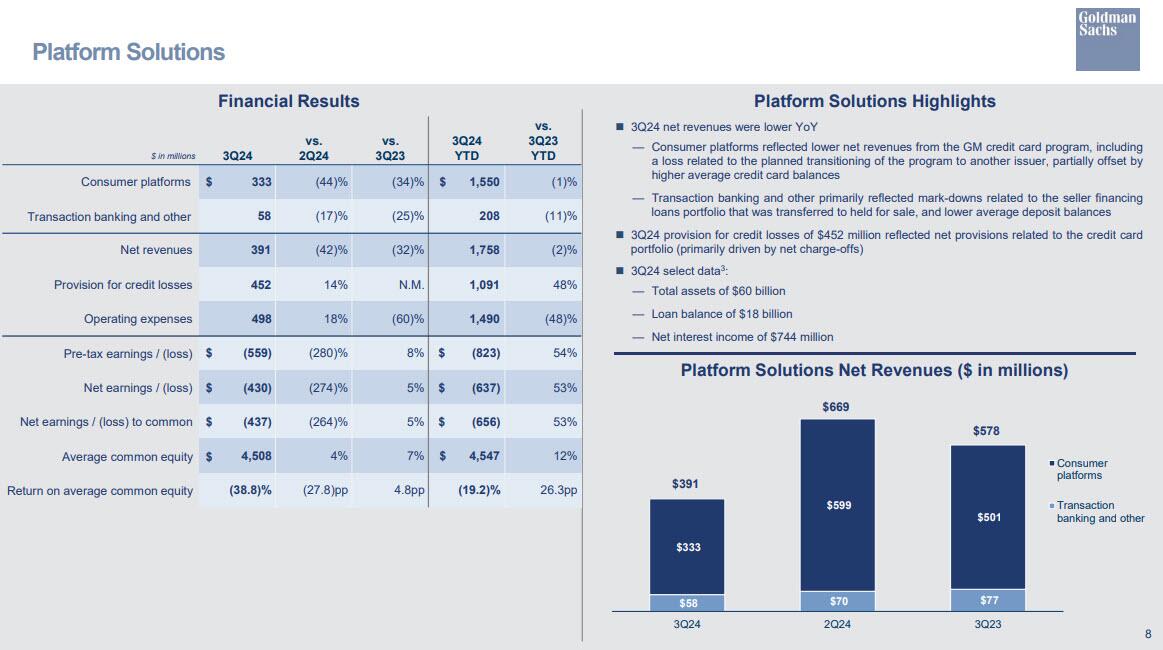

Total assets under supervision for Goldman’s wealth management group rose $169 billion to a record $3.10 trillion, driven by inflows across all asset classes, particularly in liquidity products and fixed income assets. The group also benefited from net market appreciation primarily in fixed income and equity assets.(Click on image to enlarge) The consumer-platforms business, dubbed the bad bank within Goldman, recorded a 32% drop in revenue to $391 million, driven by the GM card exit and resulting in a pretax loss of $559 million.

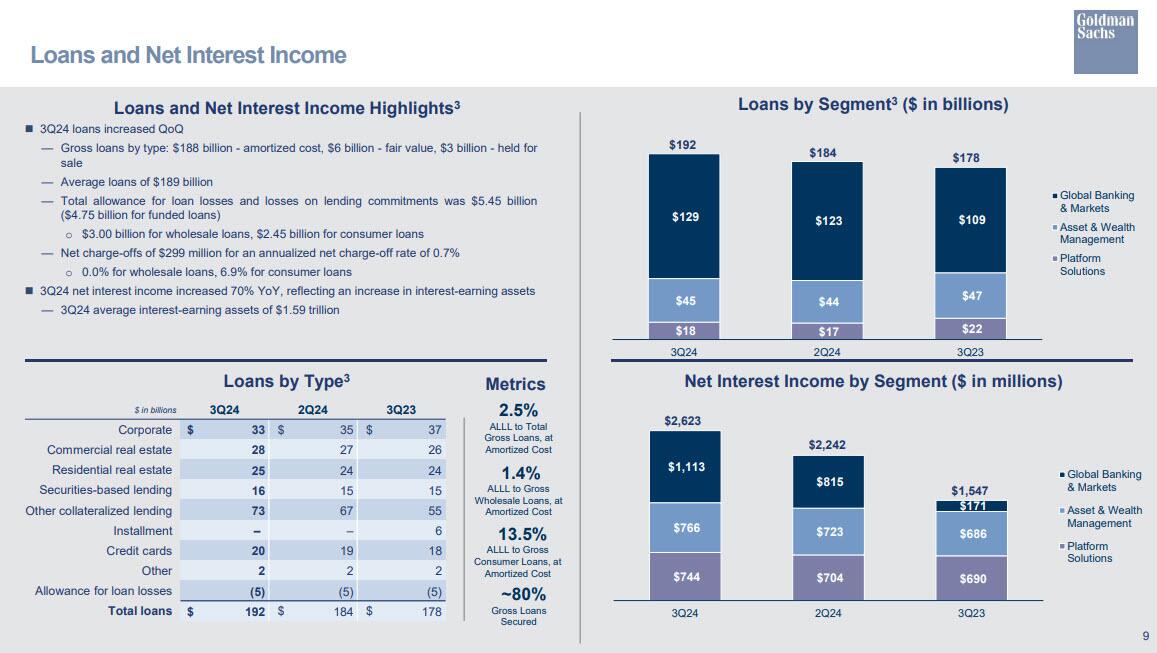

The consumer-platforms business, dubbed the bad bank within Goldman, recorded a 32% drop in revenue to $391 million, driven by the GM card exit and resulting in a pretax loss of $559 million. The bank’s net interest income rose a whopping 70% YoY to $2.62 billion, smashing estimates of $1.85 billion; the bank reported that in Q3, its average interest-earning assets were $1.59 trillion.(Click on image to enlarge)

The bank’s net interest income rose a whopping 70% YoY to $2.62 billion, smashing estimates of $1.85 billion; the bank reported that in Q3, its average interest-earning assets were $1.59 trillion.(Click on image to enlarge) Investors have sent Goldman shares higher this year as the bank abandoned major parts of its consumer-banking push and positioned itself to benefit from a rebound in investment banking. As Bloomberg notes, across Wall Street, big banks are showing they can fend off headwinds in their retail businesses from the reduction in interest rates, while highlighting the potential for increased dealmaking that would lift fees across the industry. But few are doing it as well as Goldman, whose shares have posted the biggest gain among the top US banks this year, advancing 36%, and they reached an all-time high on Monday. The stock jumped 3.3% at 8:03 a.m. in early New York trading.(Click on image to enlarge)

Investors have sent Goldman shares higher this year as the bank abandoned major parts of its consumer-banking push and positioned itself to benefit from a rebound in investment banking. As Bloomberg notes, across Wall Street, big banks are showing they can fend off headwinds in their retail businesses from the reduction in interest rates, while highlighting the potential for increased dealmaking that would lift fees across the industry. But few are doing it as well as Goldman, whose shares have posted the biggest gain among the top US banks this year, advancing 36%, and they reached an all-time high on Monday. The stock jumped 3.3% at 8:03 a.m. in early New York trading.(Click on image to enlarge) Full Goldman investor presentation ().More By This Author:

Full Goldman investor presentation ().More By This Author: