Apple’s stock surged 7% after reporting flat earnings and revenue growth. Investors didn’t seem to mind that Apple is struggling to generate growth. What mattered more to Apple investors was their pledge to buyback $110 billion of stock. According to by the Wall Street Journal, S&P 500 companies completed $181bn of buybacks in the first quarter, up 16% from the first quarter a year ago. The quote below from the article caught our eye.

“Corporate America thinks their fundamentals are fine. They’re not worried about rates, not worried about their balance sheets,” said Jeffrey Yale Rubin, president of Birinyi Associates. “If people that know the companies the closest are comfortable buying their stock, why wouldn’t I be?”

Rubin’s quote is very misleading. Companies buyback their stock for two reasons. First, they have excess cash and would rather pay it back to shareholders via buybacks as opposed to dividends. Second, executives are paid heavily in stock options, so pushing the stock price higher is in their best interest. Not only does it personally reward them, but a higher stock price is now the standard for executive performance. Unlike Rubin’s sentiment, stock buybacks are not really a function of fundamentals and confidence. For most companies, it comes down to a decision of how to spend excess cash. Buybacks help executives and current shareholders. Investing it back into the company results in future earnings growth and rewards long-term investors.

What To Watch Today

EarningsEconomy

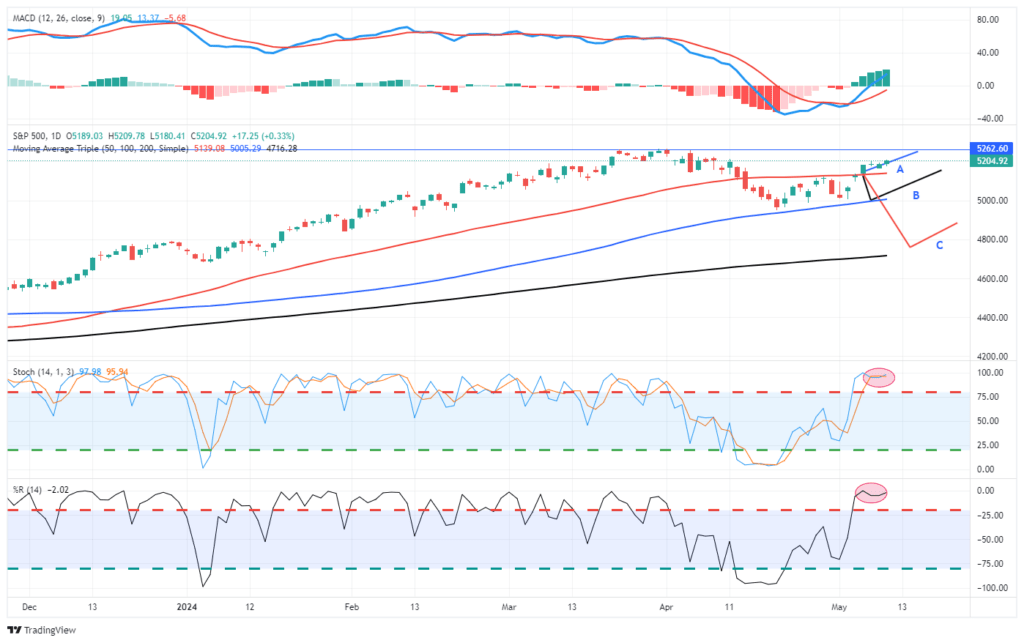

Market Trading Update

I laid out three paths for the market to follow. So far, the market has followed Path A, which we assigned the highest possibility in the short term. The market is overbought, as the rampant reversal in stocks has led to a sharp rise in investor bullishness. A pullback to support would be both logical and beneficial to increase equity exposure in portfolios as needed.(Click on image to enlarge) Next week, the all-important inflation report will be released. If weaker than expected, it could lead to a continued push higher in both stocks and bonds as a bullish repricing for rate cuts occurs. There are a ton of Fed speakers today ahead of that report, which could move stocks as well. However, as noted, with markets overbought, be patient and look to “buy the dip” for now.

Next week, the all-important inflation report will be released. If weaker than expected, it could lead to a continued push higher in both stocks and bonds as a bullish repricing for rate cuts occurs. There are a ton of Fed speakers today ahead of that report, which could move stocks as well. However, as noted, with markets overbought, be patient and look to “buy the dip” for now.

Is Phantom Debt Keeping Consumption Strong?In yesterday’s , we wrote:

With limited income and savings, consumers often rely on credit card debt. As a testament to the growing economic headwinds facing consumers, credit card debt outstanding is now growing above pre-pandemic trends.

ZeroHedge recently wrote , which adds more to our analysis of personal consumption. The puzzle is that consumers are financially exhausting their means to spend, yet personal consumption is seemingly doing well. The culprit could be phantom debt, as Bloomberg calls it. It may also mean that untraditional debt is warping our understanding of consumers’ spending ability. Per ZeroHedge:

But staggering as the mountain of household debt may be, at least we know how huge the problem is; after all the data is public. What is far more dangerous – because we have no clue about its size – is what Bloomberg calls “Phantom Debt“, and we have repeatedly called Buy Now, Pay Later debt. How much of that kind of debt is out there is largely a guess.

The article states that phantom debt masks consumers’ financial health and ability to consume. The problem for economists is that disclosure requirements for buy-now-pay-later loans and other types of phantom debt are poor. Furthermore, credit agencies may avoid reporting the data as it “could harm consumers’ credit scores, which are key to securing mortgages and other loans.” The second graph below shows that many who take buy-now-pay-later loans are not financially in good shape.The takeaway is that the consumer may have more ability to spend than we believe, but this added ability only weakens their financial health, thus negatively impacting their ability to spend in the future.

More On Q1 Earnings

Yesterday’s Commentary noted a common theme in the market’s reaction to Q1 earnings reports. Specifically, companies reporting bad earnings in Q1 were penalized more than is typical. To wit, “conversely, companies that missed got penalized much more than usual, underperforming the S&P 500 by 5.1% versus the historical average of 2.4%.”SocGen provides more interesting data on Q1 earnings. According to their data, over three-quarters of those who reported earnings beat EPS expectations by +1 standard deviation or more. While that is good news, the not-so-good news is that only 60% of companies beat market expectations on their revenues. This is the lowest percentage in the last year. In other words, higher margins and financial engineering are making earnings look better than they otherwise would be.

Tweet of the Day

More By This Author:The Investment “Holy Grail” Doesn’t ExistEconomic Headwinds Are Starting To GustCould ACDC Bring Needed Growth To Apple?