Image Source:

Image Source:

The market finally took a much-deserved breather on Wednesday following a scorching rally. There was little doubt that plenty of stocks were getting overheated after the run that began at the end of October got sent into overdrive following the Fed’s recent dovish turn.Stocks then ripped higher through early morning trading Thursday as buyers stepped in and bought the first big dip heading into the official Santa Claus rally period. Wall Street could, no doubt, experience more selling in the days and weeks ahead since markets never go straight up.Thankfully, lower interest rates and the expectations of Fed rate cuts change the math on cash and bonds. More investors are also positioning themselves to be on the right side of a possible extended rally in 2024—especially if they missed out this year. Plus, the recent run featured nearly every corner of the market and not just large-cap tech.Investors might want to consider buying stocks outside of technology heading into 2024. Some might also want to focus on stocks that are trading at solid valuations at a time when much of the market is rather overheated.

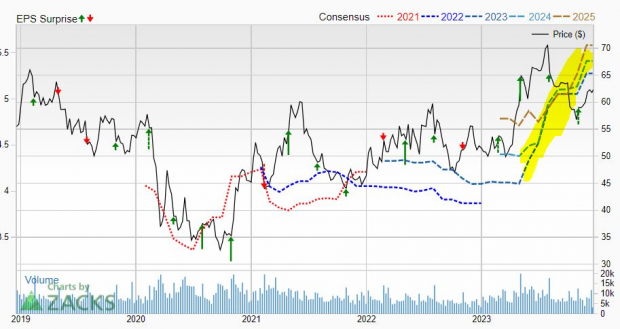

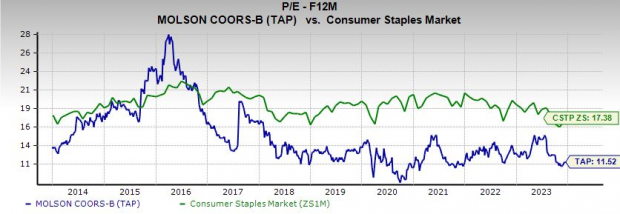

Molson Coors ( – )Molson Coors is a beer titan that competes alongside Anheuser-Busch InBev ( – ), Constellation Brands ( – ), and others in the U.S. and around the world. Molson Coors’ growing portfolio includes Coors Light, Miller Lite, Molson Canadian, Vizzy Hard Seltzer, and much more. Molson Coors said in early October that it achieved the goals it set in 2019 under its “Revitalization Plan” to post consistent sales and revenue growth, and it laid out plans for more growth in the years ahead. Image Source: Zacks Investment ResearchThe firm’s core brands have gained traction and it has found success in its expansion outside of beer into whiskeys, energy drinks, and other non-beer areas. Molson Coors topped our Q3 EPS estimate and boosted its guidance.TAP’s adjusted earnings are projected to climb by 29% this year on 9% higher revenue and then post additional growth next year. TAP’s recent upward earnings revisions extend its year-long run of improving earnings outlooks that helps it land a Zacks Rank #1 (Strong Buy) right now.The company’s improving business helped TAP’s board authorize a new $2 billion share repurchase program earlier this year. TAP’s dividend yields 2.7% at the moment. And CEO Gavin Hattersley stressed last quarter that Molson Coors was upbeat that it will hold onto its market-share gains following the Bud Light boycott.

Image Source: Zacks Investment ResearchThe firm’s core brands have gained traction and it has found success in its expansion outside of beer into whiskeys, energy drinks, and other non-beer areas. Molson Coors topped our Q3 EPS estimate and boosted its guidance.TAP’s adjusted earnings are projected to climb by 29% this year on 9% higher revenue and then post additional growth next year. TAP’s recent upward earnings revisions extend its year-long run of improving earnings outlooks that helps it land a Zacks Rank #1 (Strong Buy) right now.The company’s improving business helped TAP’s board authorize a new $2 billion share repurchase program earlier this year. TAP’s dividend yields 2.7% at the moment. And CEO Gavin Hattersley stressed last quarter that Molson Coors was upbeat that it will hold onto its market-share gains following the Bud Light boycott. Image Source: Zacks Investment ResearchTAP stock has climbed nearly 40% over the last three years to blow away Constellation’s 10%, Anheuser-Busch InBev’s -10% decline, and the wider Zacks Consumer Staples sector’s -6% dip. Molson Coors stock has climbed 19% in 2023. Yet it currently trades over 13% below its summer highs and 45% below its all-time highs.On the valuation side, TAP trades at a 60% discount to its peaks, 15% under its 10-year median, 35% below BUD, and at a 33% discount to the Consumer Staples Sector at 11.5X forward 12-month earnings.

Image Source: Zacks Investment ResearchTAP stock has climbed nearly 40% over the last three years to blow away Constellation’s 10%, Anheuser-Busch InBev’s -10% decline, and the wider Zacks Consumer Staples sector’s -6% dip. Molson Coors stock has climbed 19% in 2023. Yet it currently trades over 13% below its summer highs and 45% below its all-time highs.On the valuation side, TAP trades at a 60% discount to its peaks, 15% under its 10-year median, 35% below BUD, and at a 33% discount to the Consumer Staples Sector at 11.5X forward 12-month earnings.

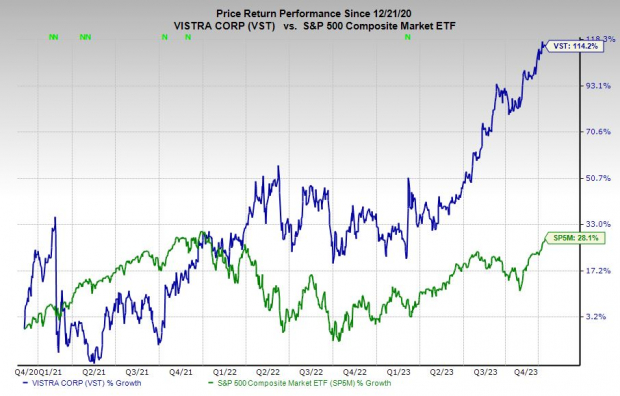

Vistra Corp. ( – )Vistra is one of the leading integrated retail electricity and power generation companies in the U.S. The Irving, Texas-based firm currently serves approximately 4 million residential, commercial, and industrial retail customers across 20 states, including six of the seven competitive wholesale markets in the country.Vistra is one of the largest competitive electricity providers in the country, with a wide-ranging portfolio that features nuclear, solar, battery energy storage facilities, and natural gas. Image Source: Zacks Investment ResearchAll four of the brokerage recommendations that Zacks has for Vistra are “Strong Buys.” And its dividend yields 2.3%. VST is also attempting to close its planned acquisition of Energy Harbor. Vistra announced back in March its plans to boost its zero-carbon generation portfolio via the purchase of Energy Harbor, including its 4,000-megawatt nuclear generation fleet and retail business of roughly 1 million customers.Vistra shares have climbed by 114% in the past three years vs. the Zacks Utilities sector’s 5% drop. This run includes a 62% surge in 2023 that’s seen it post fresh highs along the way. Despite the climb, it still trades below its average Zacks price target. On top of that, Vistra trades at a 40% discount to the Zacks Utilities sector at 8.1X forward 12-month earnings despite its huge outperformance. Plus, its PEG ratio, which factors in long-term EPS growth, sits at 0.13 vs. its industry’s 1.9.

Image Source: Zacks Investment ResearchAll four of the brokerage recommendations that Zacks has for Vistra are “Strong Buys.” And its dividend yields 2.3%. VST is also attempting to close its planned acquisition of Energy Harbor. Vistra announced back in March its plans to boost its zero-carbon generation portfolio via the purchase of Energy Harbor, including its 4,000-megawatt nuclear generation fleet and retail business of roughly 1 million customers.Vistra shares have climbed by 114% in the past three years vs. the Zacks Utilities sector’s 5% drop. This run includes a 62% surge in 2023 that’s seen it post fresh highs along the way. Despite the climb, it still trades below its average Zacks price target. On top of that, Vistra trades at a 40% discount to the Zacks Utilities sector at 8.1X forward 12-month earnings despite its huge outperformance. Plus, its PEG ratio, which factors in long-term EPS growth, sits at 0.13 vs. its industry’s 1.9. Image Source: Zacks Investment ResearchVST’s revenue is projected to soar 47% this year and another 11% next year. Better yet, Vistra is projected to swing from an adjusted loss of -$2.94 a share to +$3.79 per share this year and then surge another 23% next year. Vistra’s upbeat earnings outlook helps it grab a Zacks Rank #2 (Buy) right now. More By This Author:

Image Source: Zacks Investment ResearchVST’s revenue is projected to soar 47% this year and another 11% next year. Better yet, Vistra is projected to swing from an adjusted loss of -$2.94 a share to +$3.79 per share this year and then surge another 23% next year. Vistra’s upbeat earnings outlook helps it grab a Zacks Rank #2 (Buy) right now. More By This Author:

2 Great Value Stocks To Buy For 2024